Paper and graphics: supply chain sentiment

The expectations of entrepreneurs in the graphics/converting sector, taken from a study by the Federation, show some modest improvements. Including on the domestic market.

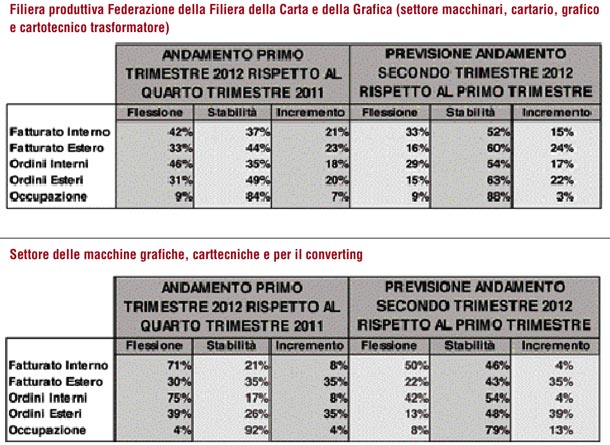

The study conducted among member concerns in the Paper and Graphics Industry Federation supplies some useful elements for understanding the dynamics of the graphics, paper production and converting machinery, paper and board production, graphics and paper converting sectors during the crisis, by revealing the sentiment of these entrepreneurs concerning the immediate future, which is to say their expected turnover and orders on the domestic and foreign markets, and an estimate of their employment capacity. The responses provided at the end of the quarter, compared with those concerning the previous quarter, and commented on by the study’s research coordinator, Prof. Alessandro Nova of the Bocconi University. Here are the results for April, May and June 2012, with a focus on the machinery and paper production sectors.

Trends of the industry. Among paper/graphics/converting operators, both pessimists and optimists are declining; expectations for stability have increased (52% against the 37% during the first months of the year). This stability is conditioned, Nova warns, both by tensions generated on the domestic market by maneuvers to bring down the deficit and by a slowdown in growth in foreign markets, where even the most dynamic economies like China and Brazil are losing ground.

Machinery. Some glimmers of light can be seen in the expectations of graphics, paper production and converting machinery manufacturers. Indeed, there have been increasingly brighter expectations concerning exports, where optimists outnumber pessimists both in terms of turnover (35% against 22%) and orders (39% against 13%). But domestic market expectations have also improved, even though more still expect a drop more than growth, both in turnover (50% against 4%) and in orders (42% against 4%). Employment, for 92% of respondents, looks to remain more or less stable.

Paper production and converters. This sector largely “held fast” in 2011, with an end of year slowdown and bleak premonitions in early 2012, followed by improvement in the second quarter. The foreign market in particular is expected to improve, where optimists exceed pessimists both in forseeing turnover increases (27% against 14%) and in expecting higher numbers of orders (32% against 14%).

The complex situation of the domestic market, on the other hand, led to negative expectations for turnover (32% against 20% of concerns with positive outlook) and orders (28% against 12%); it should be noted, in this case, that a slight improvement over the previous quarter has taken place, while the share of concerns who expect a drop in employment (12% against 8% at the beginning of the year) has increased, while the remaining 88% of operators see this component remaining stable.