Considerations on glass packaging – Data 2013

5000 years of history for a material accidentally discovered by the ancient Phoenicians: glass has experienced (and is experiencing) numerous innovations, in particular as regards its function as packaging.

During the long presence on the market, glass bottles and jars have been subject to strong competition from other types of packaging, particularly since the seventies, up to losing position during the eighties.

The glassworks however have reacted by implementing strong communication campaigns to highlight the characteristics of the material, not without innovation in terms of shapes and colors, with a view to greater customization of bottles, jars and flacons, depending on the type of product, the brand, its origins ... This is the case whether one is dealing with containers for beverages and perfumes or vegetable preserves. Much focus has been placed on the complete recyclability of glass and on the benefits related to the saving of raw materials required for production.

The market

The glass packaging offer is extremely varied, both in terms of formats and in terms of outlet areas. The “classic” classifications include bottles, jars, glass flacons and tubular glass packaging, ie ampoules and vials.

The glass sector, even allowing for the effects of the ongoing crisis in 2013, showed an increase of 1.3% in production expressed in volume due to the growth of exports (+ 7.3%). Down 1%, on the other hand, domestic consumption, due in particular to a drop in imports (down by about 10%).

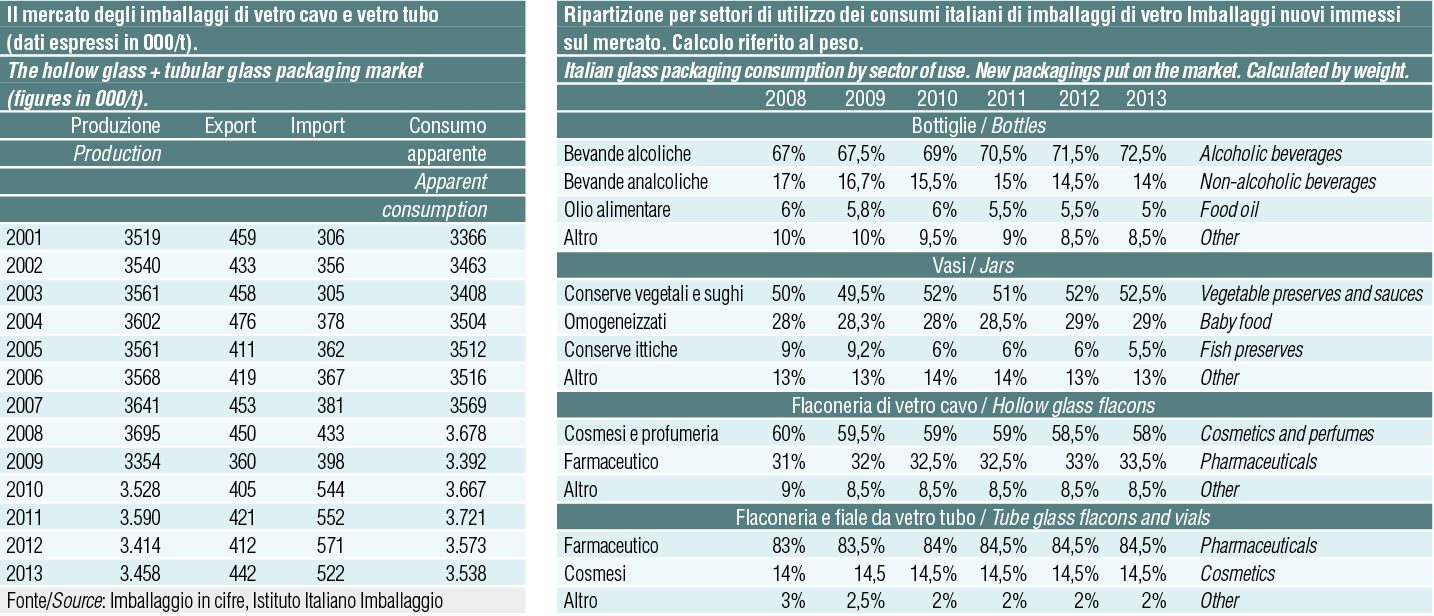

Giving an overall breakdown of glass packaging, 88.6% is comprised by bottles, 7% by jars, 4% hollow glass flacons and 0.4% tubular glass vials and ampoules.

Sector uses

Bottles and jars are used primarily in the liquid food and food preserve areas. Flacons (jars, bottles and flacons) are used in the pharmaceutical and cosmetic/perfumery fields, while tubular glass packaging is mainly used in the pharmaceutical sector.

Bottles. With reference to the new bottles on the market, their use in the liquid food area is fairly widespread.

The main outlet area of hollow glass bottles is that of alcoholic beverages (69%), where wine absorbs by far the highest proportion (48%): despite competition from other types of packaging, this container benefits from strong exports, where premium wines essentially packed in glass hold pride of place. The glass bottle is also widespread in the brewing industry (which however has to face up to cans and kegs) and “reigns supreme” with spirits and vermouth. The area of non-alcoholic beverages absorbs a share of 16.6%, where mineral water accounts for 9.5%: Here too glass finds itself competing with other forms of packaging, in particular with the PET bottle (accounting for 79%).

Another interesting area of application is that of fruit juices, where the single-dose bottles holds pride of place. The share of glass though is seen to be declining, in the face of competition from polylaminate cellulose containers and, aboveall, the development of a PET bottle (which is eroding space with both types of packaging).

The packaging of olive oil in glass amounts to share of 5.3%: predominant on the domestic market, as regards exports it has to compete with tin cans as well as PET bottles. Other fields of use of glass bottles (9.1% global share) are vinegar, tomato puree, cordials etc.

Jars. Glass jars are used 32% for packing vegetables, including the category of ready-made sauces and olive and vinegar pickles. 24.5% of jars are earmarked for baby food, 8% for the field of fish preserves (that have a growing market share) and 4% of use is accounted for by chocolate cream spreads. The remaining 31.5% is destined for a host of other foods (olives, spices, jam and so on). Its main competitor is the tinplate or aluminum can, but in recent times polylaminate cardboard containers and polylaminate flexible converter bags are enjoying ever greater success, to be considered in the coming years the most feared competitors of the glass jar.

Flacons and tubular glass. The perfumery-cosmetics sector absorbs about 83% of production, pharmaceuticals 15%, while the remaining 2% involves other areas of use. As for the tubular glass for packaging the main area of use is the pharmaceutical industry with a share of over 80%.

Plinio Iascone

Istituto Italiano Imballaggio