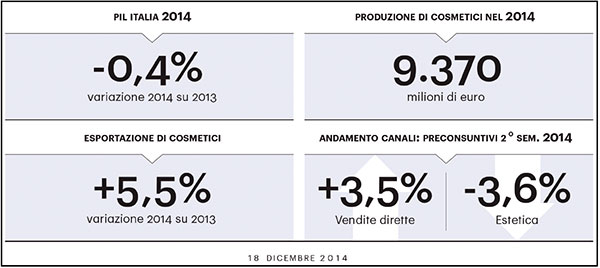

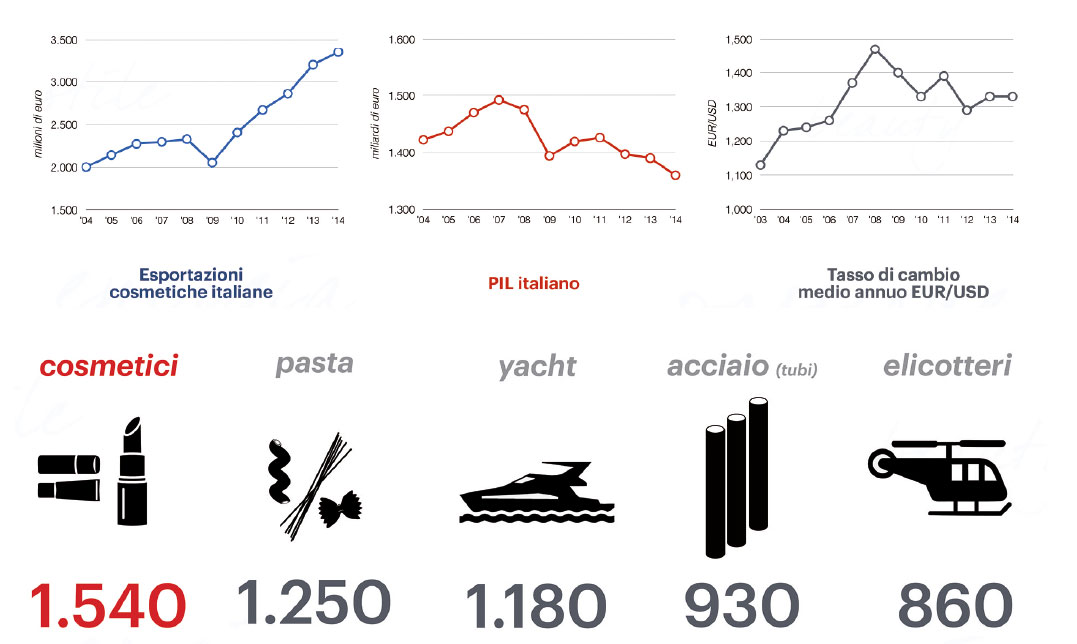

Exports at + 5.5% for Italian cosmetics

Multichannel, new forms of distribution and purchasing habits redraw the sector domestic market.

The closure indication for 2014 and the trend expected for the first months of 2015 offer a broadly neutral picture for the Italian cosmetics sector, as emerges from the regular market survey made by the Cosmetica Italy Study Centre, now in its twenty-eighth formulatioin and presented December 18 last year. The macro-economic data, in comparison with the economic and the Italian industrial scenario, are again seen to be satisfactory and partially inelastic to the prevailing economic crisis, as confirmed by the industrial indicators drawn up.

Inevitably the industry average accounts for differing situations, both between the different channels and within the same, with an impact on the global market value which, at the end of 2014, reached 9,500 million euro, with a slight contraction generated by reduction of the average value: More or less the same amounts are being bought, but at lower prices.

On the production side, the value of sector sell-in turnover, just under 9,400 million euros, suffers from a static domestic demand, down 1.4 percentage points, while it is still bolstered by exports which, while having slowed, grew 5.5% at the end of 2014.

At any rate competitive. The results underscore the extraordinary competitive capacity of the Italian cosmetics industry and the reaction to the economic downturn.

Once again it is the foreign component of demand driving the growth in turnover while the global market value touches 9,500 million euro, with a slight decrease (-1.4%) generated by the reduction of the average value: Practically speaking more or less the same amounts are being bought, but at lower prices.

Phenomena such as multi-channel, the new forms of organized distribution – monobrands first and foremost - the lesser attendance of professional salons and the use of new buying habits with e-commerce and direct sales characterize the domestic market of recent years.

The shifting between the various distribution channels is to the detriment of the hair and beauty salons. For the former, compared with a second half of 2014 showing a drop of 2.9%, further declines for the first half of 2015 (-2.4%) are not expected.

Similarly, the beauty centers recorded a market value of close to 240 million euros with an optimistic slowing of the downturn seen for the first months of 2015 (-3%).

Perfumery is more prone to the changes tastes and attitudes of consumers: Also in the second half of 2014 consumption dropped by 2.5% showing an average annual drop of 2.7%. A further decline of three percentage points for the first half of 2015 is expected, with the gap widening between the static nature of traditional perfumeries and the successful dynamics of the organized chains and small distribution companies.

Large retailers in turn confirm their position as the most important sales channel for cosmetics, with a value close to 3,800 million euros. To be highlighted the different situations in the various types of distribution and surface, with specialized spaces defined “home-toilette” putting in a particularly positive performance in holding their own. The rationalization of demand towards the pharmacy channel has led to weak growth of 0.5% for the second half of 2014 and the forecasts for early 2015 of +1%. Herbalist shops are one of the most dynamic traditional channels, with an average annual growth of 2.4% and a forecast of + 3% for the first half of 2015. These positive trends are due to the growing attention for “naturally derived” cosmetics, also sought by consumers in channels not directly associated with the eco/green sector.

Direct sales are seen to be ever closer to the changing needs of consumption compared to traditional channels and register annual closure forecasts close to 3%, with sales volumes close to 550 million euros. Contractors’ indication are undoubtedly auspicious across all channels: + 3.5% in the second half of 2014, + 3% the forecast for the first half of 2015.

«The Italian cosmetics sector confirms its inelastic nature in the face of negative trends, corroborating its position as an Italian manufacturing excellence. Its competitivity on foreign markets is also confirmed as a qualifying element for the Italian cosmetics industry and essential growth opportunity for the companies in the sector. This competitivity can without a doubt be attributed to a constant resorting to investments in innovation and research, alongside a highly qualified production capacity» President of Cosmetica Italia Fabio Rossello commented on this count, in illustrating the results for 2014 and the forecasts for 2015 for the beauty segment.