Flexible packaging – Data 2013

Featuring complex structures, flexible packaging enables the design of combinations of different materials (cellulose, plastic, aluminum foil or metallization) taking into account both the characteristics of the product to be contained, as well as the shelf life which must be guaranteed. This peculiarity is its main strength.

That of flexible converter packaging is one of the few areas of the “packaging” market that, in reference to its “lifecycle”, continues to express a trend showing progressive and interesting growth.

If at first growth was mainly driven by the erosion of shares of other types of packaging, in recent times it is derived by the inclusion in new areas: chilled or frozen ready meals, fresh-cut convenience fruit&vegetables, the marketing of pre-packaged and pre-weighed fresh food, the handling of fresh fish products from aquaculture centers to the point of sale etc..

Another significant aspect of the sector is the strong propensity to export that, on average, accounts for 44-47% of production.

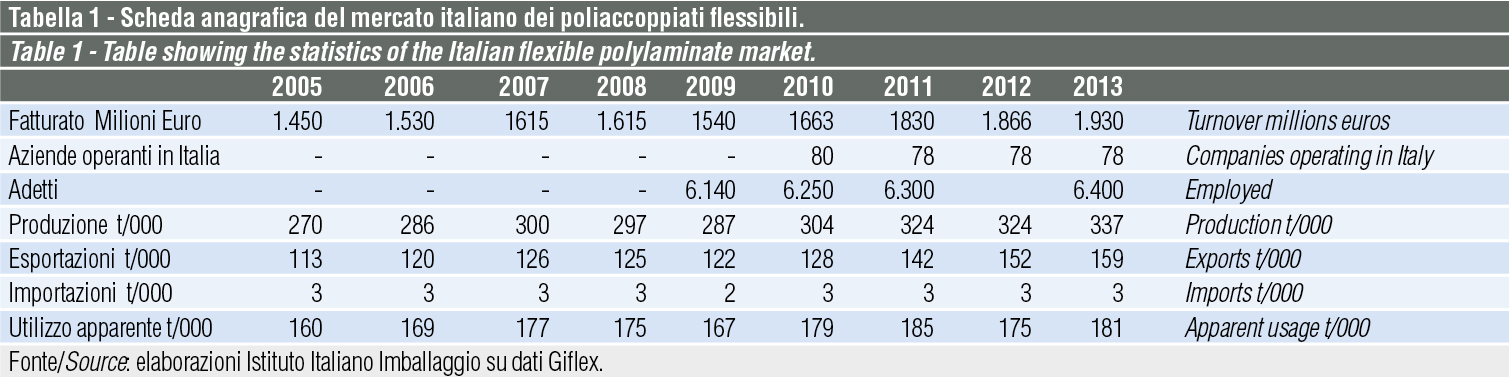

Figures and market characteristics

In 2013 the “flexible converter” packaging sector expressed a domestic demand of 181,000 t (+3.4% compared to 2012).

Exports are definitively positive (+4.6%, equivalent to 47% of production). In this regard, we recall that the Italian flexible packaging manufacturers have always expressed a strong export orientation, aiming to provide quality and service to the customer (their true strengths), and that some producers export more than 70% of their output.

The favorable trend of the two demand components has led to a growth in production of 4% in end-of-year figures.

Imports are as ever contained (1% of national consumption), but foreign competition, especially Turkish, is making itself felt.

It should also be pointed out out that, in recent years, converter polylaminates have shown a reduction in weight while offering the same performance.

This process is the result of fruitful research, aimed at identifying new materials and production techniques. Over the last few years, the use of the cellulose component and that of aluminum foil has been reduced (in the latter case, resorting to metallization). These changes were made possible thanks to the design of multilayer plastic, which fulfils the functions performed by the cellulosic sheet or that of aluminum.

It is estimated that currently 82% of flexible converter polylaminates are “all plastic”, 14% are with the presence of aluminum foil and 4% with paper sheet.

Fields of application

Fields of application

Food

The food area, with a share of 90.5%, remains the main market for polylaminate flexible converter packaging.

The high spread in the food industry stems from several factors, primarily the growth of pre-weighed and pre-packaged foods - usually in a protected atmosphere, ready to use dishes in a protected atmosphere, the spread of fresh-cut convenience fruit&vegetables etc..

In the food area, with reference to sales in Italy, the most significant outlet areas are bakery products and pasta (accounting for 25.4% of overall use with fresh industrial pasta and ice cream heading the way) dairy products (cheese, yogurt, butter, etc..) that account for a share of 18%.

With regard to the dairy products area the main use is for pre-packaged and pre-portioned cheeses, both those from the producer concerns and those packed at modern distribution.

Other important areas of application are: processed and cold cut meats (8.7% in progressive growth both from industry and with products packaged at largescale retail outlets); frozen foods (7.6%); coffee (3.5%); petfood (3%).

It is precisely in this sector that flexible packaging sees interesting potential, both due to the growth in sales of petfood in its entirety and for the inclination to increase the use of flexible packaging products for packaging dry and wet products, to the detriment of other packaging solutions.

Still in the macro food area, flexible packaging has good growth potential for legume and tomato derivative preserves for horeca, creams and sauces etc.. The current market share of the “other food” segment has reached 24.3%.

Non food

In the non-food area (9.5%), the main field of application of the flexible packaging is the pharmaceutical/cosmetics sector (4.8% global share).

Household detergents are at 4.5% and in 2013 suffered a decline in consumption caused by the crisis; flexible polylaminates however continue to present good development potential due both to the trend towards replacing the cardboard case with the polylaminate bag, as well as for the progressive diffusion of washing additives in paste form.

Summing up

To conclude we can say that, generally speaking, flexible converter polylaminates still show a good growth potential, thanks to some

factors:

- the producers’ technical/commercial efficiency in capturing and transferring the customer needs onto the market;

- the limited footprint of this type of packaging;

- the combination in a single packaging item of the characteristics of different materials;

- this being the only packaging segment with a strong export orientation and significant competitiveness.

Plinio Iascone

Istituto Italiano Imballaggio