The market and packaging of coffee

Domestic consumption is down but Italy remains the fourth world coffee consumer, as well as a strong converter and exporter. And in packaging pods are on the increase.

Three quarters of the coffee produced worldwide is exported by producer countries, so the majority of consumption occurs outside the country of origin. Non-producing consumer countries import raw coffee and process it into roasted coffee, then transport it to POPs in the form of grains, powder, soluble, etc.

Three quarters of the coffee produced worldwide is exported by producer countries, so the majority of consumption occurs outside the country of origin. Non-producing consumer countries import raw coffee and process it into roasted coffee, then transport it to POPs in the form of grains, powder, soluble, etc.

Imports, on the other hand, in many cases do not correspond to domestic demand insomuch as a significant share of processed coffee is then exported again.

This is the case of Italy, which acquires unprocessed coffee mainly from five countries - Brazil, Vietnam, India, Uganda and Indonesia - roasts it and then markets most of the finished product domestically, but exports a progressively increasing portion (+10% in 2013, equaling 37% of sales). Italian export coffee thus plays an important role and is destined primarily to western Europe - particularly Germany, France and the Nordic countries - but also eastern Europe, the Arab states and the USA.

Consumption and channels

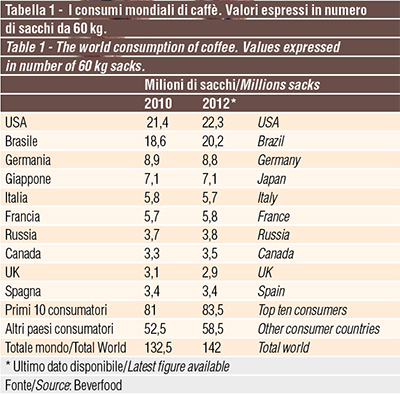

In 2012 (the latest reportable year), total coffee consumption amounted to 142 million 60 Kg bags, with a progressive growth trend. Italy consumes approximately 4% of the worldwide total, positioning itself alongside France in fourth place. There are 1,112 concerns active in coffee processing in Italy (source: Beverfood), but the first largest groups represent 70% of the market: Lavazza, Nestlè-Nescafè,Nescaffè-Nespresso; Mondelez Italia; Kimbo; Segafredo Zanetti and Illy. The concentration of supply reaches its peak in the segment of portioned coffee, in which three operators (Lavazza, Nestlè and Nespresso) absorb more than 50% of the market. Supermarket private labels, for their part, command an impressive 8% market share

In 2013, domestic consumption equaled 240,000 t, a 3% drop: this percentage compounds with the 1.3% drop recorded in 2012.

During the year in question, the main channel was retail (64%), while 21% was channeled through coffee shops and restaurants, 7% through vending machines and 8% was accounted for by single portion coffee for offices and coffee pods destined for private consumers (the latter with progressive and continuous growth).

However, Italy’s production exceeds domestic demand: approximately 360,000 tons of roasted coffee put on the market in 2013, growing 1.4% compared to 2012, thanks to the strong performance of exports (+10%). Domestic demand, on the other hand, has seen a drop of 2-3%; it should be kept in mind, on this account, that coffee is a “mature” product, with high penetration among Italian families, and consequently its performance follows the general growth trend of household consumption.

However, Italy’s production exceeds domestic demand: approximately 360,000 tons of roasted coffee put on the market in 2013, growing 1.4% compared to 2012, thanks to the strong performance of exports (+10%). Domestic demand, on the other hand, has seen a drop of 2-3%; it should be kept in mind, on this account, that coffee is a “mature” product, with high penetration among Italian families, and consequently its performance follows the general growth trend of household consumption.

It’s also important to note that in 2013, facing a drop in consumption of around 3%, espresso powder declined by 6.4% while, on the other hand, capsules grew by 19%.

Packaging trends

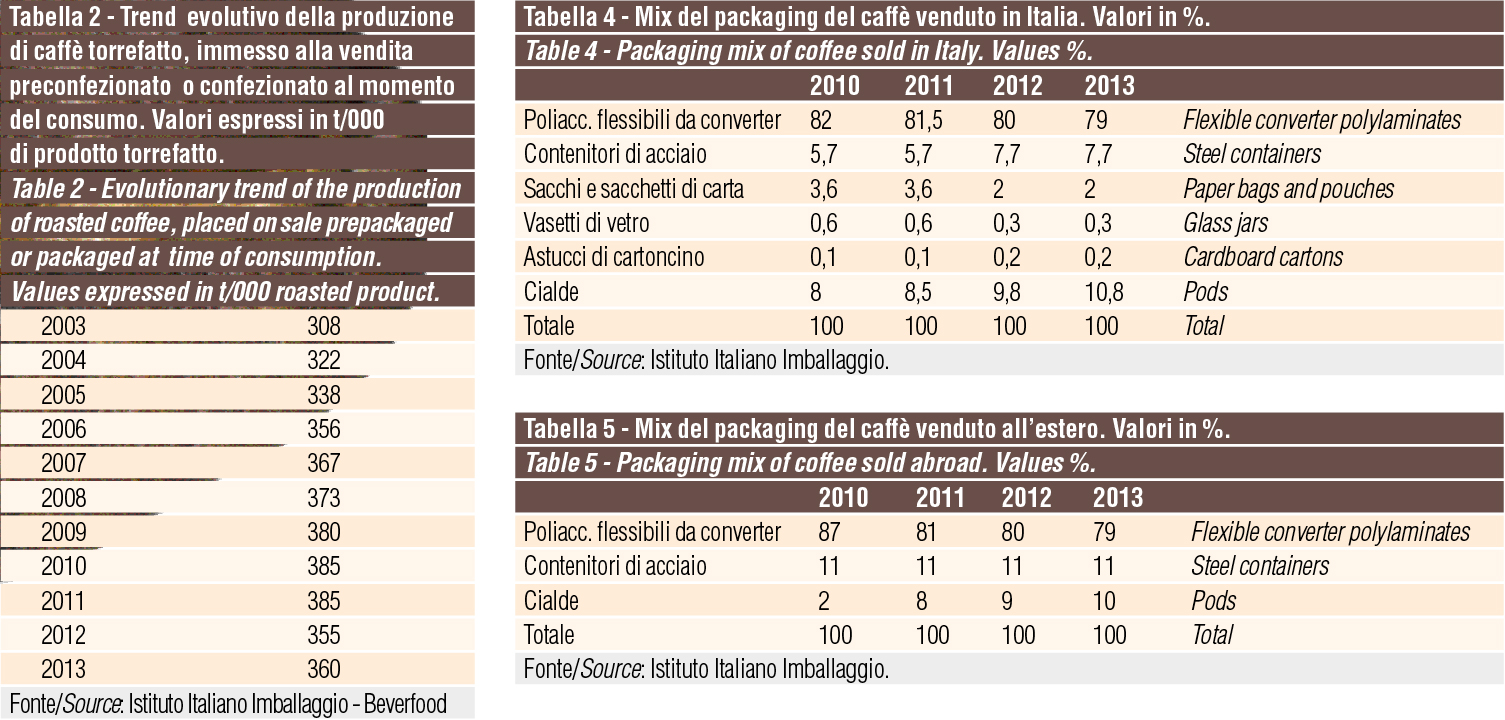

According to calculations by the Istituto Italiano Imballaggio, the types of coffee marketed in Italy show the following trends:

- sensitive growth of pods, whose share reached 9% in 2010 and 10.8% in 2013, largely to the detriment of “converted flexible polylaminate packaging”, which in 2010 represented 90% of the market and in 2013 dropped to 79%;

- tin packaging: cans or containers for bars represent 7.7% of the total;

- paper bags, used for selling loose coffee grounds in special POPs, reached 2%;

- glass jars and card boxes represented 0.5%.

Converted flexible polylaminate packaging, which remains the most commonly used packaging type, can be divided into 250 g packs (90%) and 500 g formats (10%); multipacks containing two or four 250 g bags and clusters containing two 250 g packs are very common.

Tin packaging, on the other hand, can be divided into 250 g units, for families, and 3 kg containers for bars.

These packaging types are also joined by plastic or cellulose cups used in vending machines or offices equipped with their own “machines”.

Plinio Iascone

Istituto Italiano imballaggio