The packaging sector – Data 2012

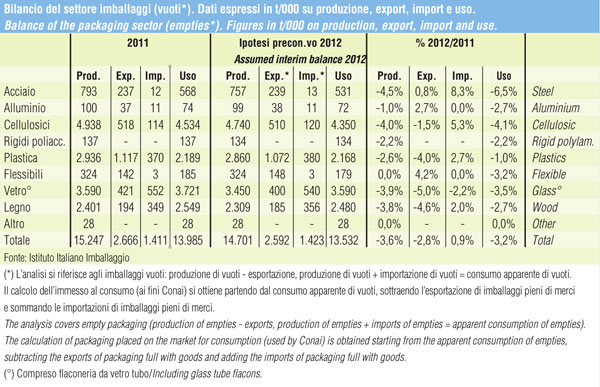

Based on early estimates, 2012 marks a net worsening of the situation compared to 2011 (*): total packaging production fell by 3-4%, exports dropped 2.8-3%, imports increased slightly, and domestic demand fell 3-3.5%. The growth trends refer to values in weight.

The negative growth figure concerns all eight sectors of the packaging industry.

Steel packaging evidences a possible 4.5% drop in production, and one of 6.5% in visible use; trade increased.

Aluminium packaging should lose ground in relation both to production and domestic consumption; exports grew, while imports remained stable.

Cellulosic packaging presents shrinkage both in production and in visible consumption. Exports dropped, imports grew.

Note

* A reminder that the packaging industry ended 2011 with a 0.7% drop in production (values in weight). Turnover, at 28.579 billion euro, grew by approximately 11%, in part destined to compensate the considerable increase in raw materials costs during the first months of the year.

Exports saw positive growth, totaling 3% overall; imports also grew, at 3.3%.

Domestic demand dropped by 1%.

The recession that affected the sector was concentrated, as in the manufacturing sector in general, in the last months of 2011.

Rigid cellulosic polylaminates show, for the first time in many years, a drop in consumption.

Plastic packaging should have ended the year with a 2-3% drop in production, caused by a contraction in exports and domestic demand; imports rose slightly.

Flexible packaging for converting seems to have ended 2012 similarly to the year before, thanks to positive growth in exports.

Glass packaging may have dropped production by 3-4%, due to a reduction in exports and visible consumption. Trade fell.

Wood packaging is characterized by a 3-4% drop in production, brought on by a drop in exports and domestic demand; imports rose.

Plinio Iascone

Istituto Italiano Imballaggio

For further information link to Report on the State of Packaging (1)