The plastic packaging market

Production growth trend, with particular reference to rigid packaging. This diverse macro category is made up of many product types, including bottles, tubs, blisters and pallets, as well as closures and much more.

For the second consecutive year, in 2013 the plastic packaging market closed with net shrinkage, at -1.2%, compared to -4.7% in 2012. The cause of this situation is the economic crisis that has affected Italy and other European countries in recent years.

Looking more closely, 2013 saw a 3.5% drop in exports, a 1.2% increase in imports and a rise in apparent consumption of 4%. The growth of domestic demand shows a further increase in the shares of plastic packaging.

General picture of the market

Within the plastic packaging, this analysis is particularly focused on rigid plastic. This varied category of products includes bottles, flacons, buckets, tubs, bins, blisters, honeycombs, crates, pallets, flexible tubes and closures.

Altogether, 55% of the production of this packaging type is destined for foreign markets and 45% for the Italian market. Exports show particularly significant values in two sectors: closures, which reach a share of 70%, and accessories (handles, adhesive tapes, protective materials, etc.), at 51%.

As for imports, they remain modest, although rising slightly over 2012. The greatest share of imports is that of closures, where they represent 53% and rising.

Also continuing to rise, furthermore, is the use of recycled plastics, particularly rPET. This practice has been underway for several years in the production of packaging. This trend has intensified since - having overcome the threshold of use only in non-food product packaging - recycled plastic is being used more and more commonly in the food sector as well.

Types and areas of use

Rigid plastic packaging finds countless sector applications in food products (fresh and preserved), beverages, technical products, etc.

In terms of production, this packaging type can be divided into five categories:

-bottles for food liquids, representing 30.3% of the total;

-bottles, flacons and containers for various technical non-food products (28.5%);

-honeycombs, blisters, trays and tubes (23.7%);

-closures (8.5%)

-various accessories, such as chords, handles, expanded chips etc. (9%).

Since 2011, all these product categories have felt the negative effects of the national and international economic crisis and, overall, 2013 ended with a 1% drop in production.

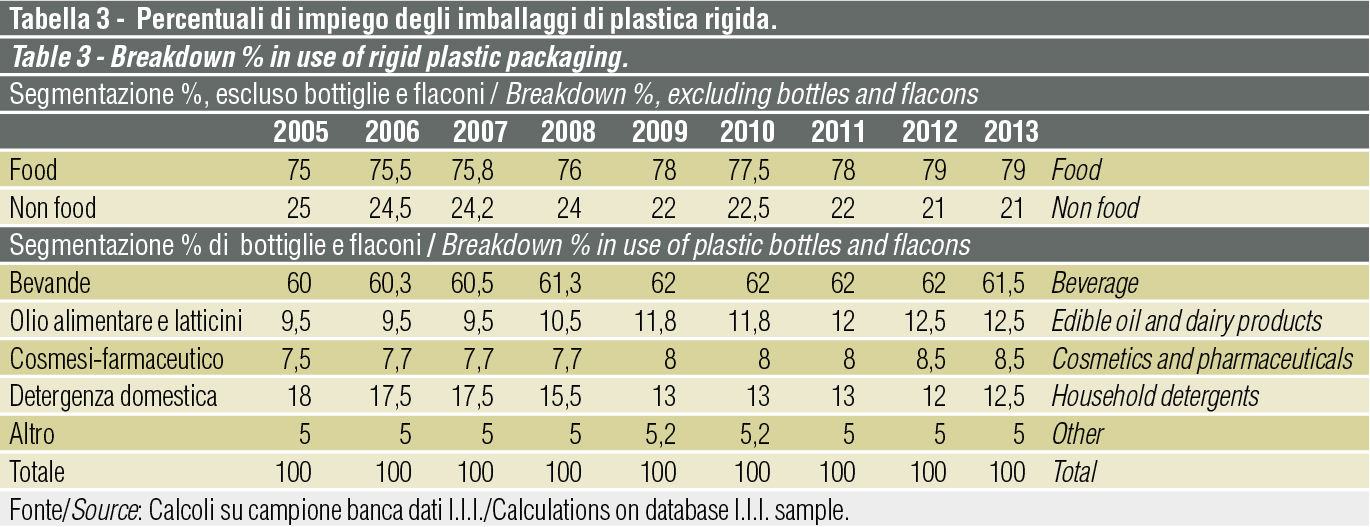

Bottles, flacons, closures. Considering the sectors of use of plastic bottles and flacons, 79% is destined for the food sector (food and beverage), while 21% is destined for the non-food sector. During the past year, as already happened in 2012, the non-food sector saw a decline, while the food and beverage industry gained ground.

In particular, during the course of 2013, plastic containers held for the most part in the beverage sector, even though competition from polylaminate cellulose containers in this area is very high.

On the rise is the use of plastic bottles in the olive oil sector destined for export and the milk sector, while flacons are holding their strong position in cosmetics/perfumes, pharmaceuticals and domestic detegence. Flacons and bottles show further potential for growth for packaging tomato sauce, wine for export, vinegar, readymade sauces and fruit juices.

Plastic closures confirm their marked tendency to erode the shares of other solutions, aboveall regarding spirits, tonic liquors, aperitifs etc.

Trays and other rigid containers. As for the other large market area of rigid containers, which includes trays, buckets, pallets, crates, flexible tubes, blisters, etc., it is estimated that 77% of these types of packaging are accounted for in the macro aggregate of food and 23% by non food.

In this area, thin wall packaging (trays, cups, blisters, etc.) tend to show the best growth rates.

The success of this packaging type is caused by the growth of portioned and pre-weighted food products, as well as ready meals displayed on refrigerated shelves, which are taking hold in supermarkets, but also in traditional distribution.

Blisters also show promising growth potential. Created to package pharmaceutical and cosmetics products, they are also gaining ground in the areas of IT accessories, stationary and metal precision tools. Also promising is the presence of the plastic crate as a transport packaging for fresh fruit and vegetable products, with both disposable and returnable versions growing significantly and progressively, having already reached a quota of approximately 60%. This spread primarily concerns the domestic market, while exports favor cardboard and wood crates, relegating plastic to third place.

Plinio Iascone

Istituto Italiano Imballaggio