Report on the state of packaging – March 2014

Quarterly packaging industry observatory. Situation at the end March 2014.

Here is a glimpse of the performance of the Italian manufacturing industry sectors where the level of packaging consumption is the most intense, divided into macro areas of food and non food.

Compared to figures given in 2013, at the time of completion of the present analysis (end March 2014), the developmental activities of the different manufacturing areas does not show substantial changes on what was published in issue 1-2/2014 of ItaliaImballaggio, page 29-31; hence readers are invited to consult that issue.

Summing things up, all sectors closed 2013 showing a downturn, despite a slight abatement of the recession registered between November and December. Expectations for 2014 are oriented towards a slow recovery, mainly bolstered by growth in exports.

Plinio Iascone

The packaging industry

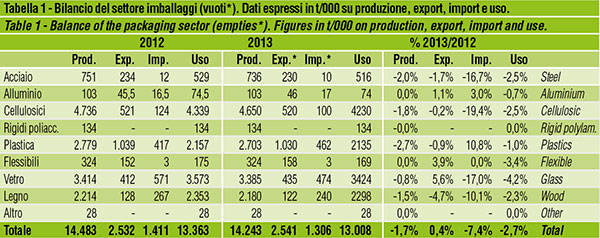

After the contractions recorded in 2012 in production (-5.1%), domestic demand (-4.6%) and foreign trade (exports -5%, imports stable at low levels ) 2013 too shows a downtrend, even though featuring a progressive abatement of the rates of degrowth.

In particular, it is estimated that:

- production showed a drop of 1.7%;

- exports showed a modest increase of 0.4%;

- imports are down by 7.4%;

- domestic demand has ended the year down 2.7%.

Hence for the third year running the packaging sector shows drop in production, in line with Italian manufacturing growth figures and the economic crisis affecting the European Union.

By analysing the performance of the various sectors of production, we find that:

- steel packaging is down by 2%;

- aluminium packaging reconfirms the low levels of activity of 2012;

- cellulose packaging is down by 1.8%;

- rigid polylaminate containers reconfirm the unsatisfactory quantities of the previous year;

- plastic packaging shows a decline in production of 2.7%;

- flexible converter packaging, thanks to the good run of exports, was able to reconfirm 2012 figures;

- glass packaging, also thanks to good export flows, should have limited the drop in production to 0.8%;

- wood packaging ended the year with a drop in the production of 1.5%.

For the Italian packaging sector, expectations for 2014 are tinged with moderate optimism, in consideration of a possible resumption of the manufacturing industry, this also including the main countries of the European Union.

For 2014 a recovery of 1.2% of domestic consumption is predicted, along with a of 3.2% increase in exports, a 3.4% increase in imports and production showing growth of 1.7%.

The information used for the calculations in this report are taken from the database of Istituto Italiano Imballaggio Istituto Italiano Imballaggio

|

The general economic situation According to Confindustria, the crisis affecting Italy (the second in six years) had ceased its vertical drop, but its negative effects are still weighing on the country. The damage caused by the long recession is worrying. Some 7.3 million people are partially or totally out of work, approximately twice the figures of six years ago. |

Plinio Iascone

Istituto Italiano Imballaggio