Food & Beverage: a Report on consumption

Focus on Italian food consumption that shows a slight recovery in quantitative terms set against a significant qualitative change, with the onus being placed on health and well-being. Data and trends taken from the full annual report drawn up by the Coop, which offer excerpts of great interest for operators in the food & packaging industry.

The Coop 2015 Report (this year too in the digital and interactive media version, available at www.rapportocoop.it) offers a snapshot of Italy and the Italians, the macro and micro differences between the different areas of the country and a comparison with what is happening in other major European countries. In particular, the report analyses the trajectories of the recovery, the legacies of the crisis and the changes in spending behavior.

The Coop 2015 Report (this year too in the digital and interactive media version, available at www.rapportocoop.it) offers a snapshot of Italy and the Italians, the macro and micro differences between the different areas of the country and a comparison with what is happening in other major European countries. In particular, the report analyses the trajectories of the recovery, the legacies of the crisis and the changes in spending behavior.

POST CRISIS AND LIFESTYLES

Before the long recession that we are still experiencing, Italian household food expenditure had never shown consistent negative fluctuations. With the crisis this too has changed, because of the tendency to save that caused a change in the mix of purchased products, seen both in the tendency to purchase lower priced products and via reducing (or eliminating) the consumption of certain goods items.

This has caused a cultural change which corresponds to a generational divide (young people spend less time preparing food, partly also due to the "feminization" of the job market) but the situation has also been affected by the arrival of many immigrants with different consumption habits.

For this reason, the reduction of food expenditure, as well as being a reaction to the effects of the crisis, might reflect the emergence of lifestyles liable to last over the years. Which, among other things, helps to explain the delay of the recovery of food consumption compared to other goods categories, and authorizes one to speculate that the procedure will be slow going for some time to come.

The changing demographic structure points in this direction. Demand is being contained partially due to overall emigration flows, which have been definitely downsized in recent years and, on another level, the health-conscious trends that have lead to a reduction in quantity of in favor of a qualitative upgrading of demand, thus reversing a process that for many years was seen to be proceeding in the opposite direction.

This path confirms the divergence of trends at a local level, where Italy's southern regions will remain more expediency orientated compared the north of the country for a long time to come.

HOW CONSUMPTION IS CHANGING: QUANTITIES

After the slight recovery observed in 2014 (+ 0.2%), food consumption in Italy could increase by 0.6% this year and 0.7% in 2016. Indeed this is a modest difference when compared to the extent of the collapse of the previous quarters, but very different from one food segment to another.

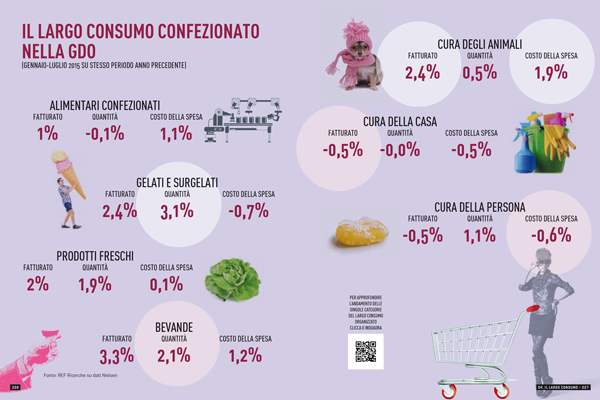

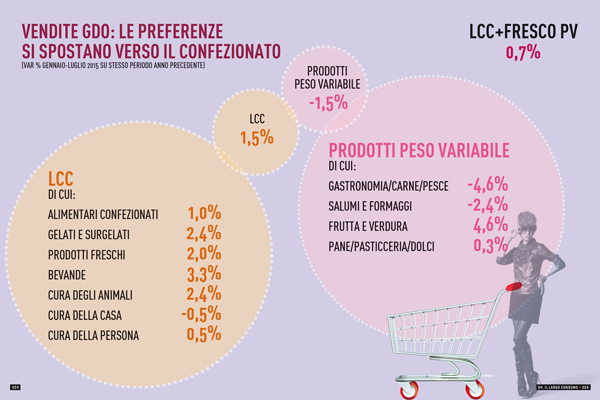

Fresh and packaged: different trends. In modern distribution, in the first half of 2015 there are early tentative signs of consolidation (about + 0.5% in value), mainly bolstered by the stability of shelf prices. This concerns packaged food (+ 1.5%), also fresh packaged foods, cold chain products, unpacked fruit and vegetables (up by more than 4%), while the fresh products of animal origin such as meat, cold cuts and dairy products still show a downturn.

Packaged products are valued for their greater service content and because they also help to reduce waste.

Beverage and hygiene. Mixed signs also from the beverage sector, where in particular the more expensive products and those that are not considered in line with a healthy and natural diet (distillates spirits and liqueurs, as well as colas and sodas) are suffering.

A further decline in sales of house-care products has also been noted, while the first signs of recovery come from personal care, thanks to the contribution of basic products (oral care and haircare products).

The hunt for discount slows down. After years of hardship and difficulties, in the first half of 2015 the trend towards saving "at any cost" (the value of saving strategies resorted to over the last three years is estimated at over 5 billion and is equivalent to some percentage points of the turnover of modern distribution) appears to have drawn to a close.

The turnaround can aboveall be seen in the reverse in the socalled "downgrading" in food purchases (the difference between on-the-shelf inflation and the actual purchasing cost), which in 2015 was halved (this trend is likely to strengthen). In parallel, for the first time in nearly a decade promotional pressure has started to drop. Today, in fact, 29% of the retail chain turnover originates in discounted products (13% of the references in the assortment) against the 29.3% in 2014, interrupting the trend that has increased promotional pressure by 18% since the years two thousand to the over 30% in the most acute stages of the recession. And, again in 2015, the growth of private label products has come to a standstill, today accounting for 18% of largescale retail chain turnover.

HOW CONSUMPTION IS CHANGING: QUALITY

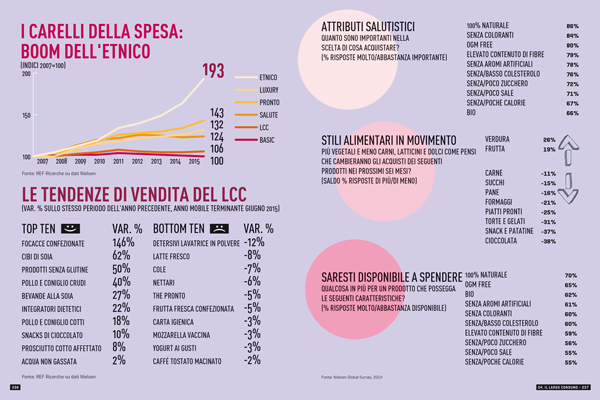

Year 2015 witnesses experimental purchasing habits, increasingly health-conscious and guided both by price as well as by the healthiness and wholesomeness of the products. In addition it includes multi-ethnic products with tastes and flavors of distant cultures, still frugal though with fewer commodities, more quality and a greater service content.

Health, catalyst of trends. In the framework just outlined, the growth of purchases of organic products and those for people with food intolerances still continues, while the purchase of high-calorie foods, such as fats and sugar, or those not consistent with more healthful lifestyles, such as alcohol, are down. The growth of ethnic food is due both to the amount of immigrants out of the total population as well as the growing mix of food cultures that is also affecting the eating habits of Italian households.

And if healthiness has become the main ingredient of our recipes (4 out of 5 consumers prefer natural, healthy and sustainable foods), it has generated a number of effects that also in various ways affect packaging and labeling supplements, be these “smart” or less so. Indeed, thanks to the increased availability of information on raw materials, processes and health-conscious attributes of food products, the post crisis consumer consciously chooses, as the occasion has it, which products to buy, how much quality he or she might bring to the dinner table and at what price. And the consumer is willing to pay more for food that promises better health: among retail products, the highest increase in sales is seen in soya based food and beverages (+ 62%), dietary supplements and gluten-free products (+ 50%).

Pleasure, but with judgement. The top ten ranking of the most loved products by Italians also includes some products that in recent years have shown some sharp rejections. Here in particular, we refer to chocolate based snacks and this is read as a positive sign of a significant return to impulse buying. However, items ill-adapted to a healthy lifestyle, like colas, nectars and sugary beverages are seen to be in a downturn.

Luxury and service. Regrouping product categories according to unique characteristics, the basic shopping trolley is seen to show a downturn (-1.7%) encompassing many products with a low unit value, with a high calorie intake compared to price.

In turn the luxury shopping trolley continues to show sustained growth (+ 4.8%), where the quality of ingredients, raw materials and certified products are considered, and which includes expensive products such as champagne, mushrooms, truffles and some ichthyic specialties.

Ready meals, that guarantee time saving and that best combine with work rhythms, are also putting in an upturn (+ 6.8%: a percentage not seen since 2010-2011).

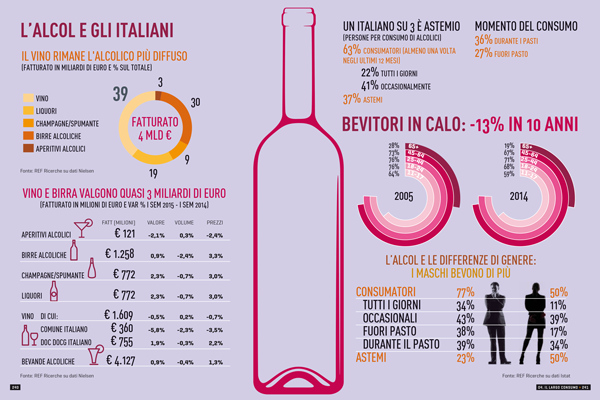

FOCUS ON ALCOHOLIC BEVERAGES

Despite what is believed, only 63% of Italians declare they consume alcohol, while the rest of the population (37%) considers itself teetotaler, compared with a European average of 24%. Against this Italians are seen to drink on a daily basis: more than one Italian in5 consumes alcohol every day. This trend, however is declining in that in a period of a decade habitual consumers have gone from 31% to 22%.

Alongside this occasional consumption and consumption beyond mealtimes is also on the increase. In other words, the intake of wine and not only is shifting from the dinner table (especially for women) to opportunities of socialization away from the home, especially among the younger and more literate part of the population. Wine is still the most popular alcoholic drink, consumed by half of Italians and 85% of daily drinkers, but here is a growing consensus for the beer, which now more than 4 out of 100 Italians drink every day. A full 4 out of 10 Italians state they occasionally consume aperitifs, ‘amari’ and spirits.

One though needs to take a closer look at quantities, turnovers and trends. Hence it can be seen that over the last year, modern distribution totalled sales of over 4 billion euro (+ 1%), featuring a drop in common wine in part offset by the upswing in consumption of DOC and DOCG certified wines, and a growth in beer consumption only bolstered by a rise in prices, while volumes are falling. Sales of appetizers are down, while figures on the consumption of champagne and sparkling wines are on the up.

PIÙ ATTENZIONE AGLI SPRECHI

If overall more than a third of production for human consumption is wasted, the value of food waste in Italy is estimated at 8.1 billion euro, which "spread" over the number of households, stands at 3.3 kg for each household lost every week on the way from the farm to the fork.

In Italy, as in general in the economically more developed countries, waste occurs both upstream, between the harvest and the first industrial processing, and downstream at the moment of consumption.

According to a recent survey by Ipsos, every month Italian households throw away about 30 euros of food into the dustbin without having eaten it, or more than € 350 on average in a year, with figures changing a lot up and down the peninsular. In a recent survey by Doxa, however, Italians are confirmed as highly attentive to avoiding waste: 59% of respondents declare little or zero waste; 38% of households admit that some waste occurs, considering it as a problem that needs to be addressed. The positive fact is that the majority of the population (as many as 7 out of 10) is aware that the fight against waste involves the behaviour and commitment of each and every one of us.

AN EXPERIMENTAL FUTURE

AN EXPERIMENTAL FUTURE

Driven by the presence of large and stable foreign communities, the spread of its restaurants and the rapid growth of ethnic retail shops (often cheaper and open after hours), foreign food consumption is evermore gaining hold in Italy.

Other trends that are becoming increasingly important are the attention to environmental sustainability and resource management, together with fears related to food adulteration and contamination. At the same time, despite a preference for the Mediterranean diet, which seems to summarize all the positive factors of food that respect people and the environment, there is a widespread readiness to try out new food items. From synthetic meat to pills, from plankton to insects.

Another important factor of change concerns distribution, or that is how we actually access food.

In the multi-channel era, most purchases will transit via the Internet (71%), with a boom in mobile transactions from smart phones and tablets, but there are even people who imagine that the spread of home automation will lead to an automatic reordering of food performed by "smart" appliances (36%). Currently, from this point of view, the gap between Italy and the other advanced countries is still wide, but so to the inclination to fill it, bolstered also by the Italian interest for innovation in food purchases. Primarily technological, but not only, as shown by the proliferation of purchasing groups, the consumption of homemade products, "zero km" and thereabouts.

RELATED ARTICLES: Food as a lifestyle choice: trends at a glance