Metal packaging – Data 2020

Sturdy, unbreakable, air-tight: these are the characteristics of steel or aluminum packaging, hence perfect for preserving food products. Market numbers per type, expressed by the sector in 2020 in Italy.

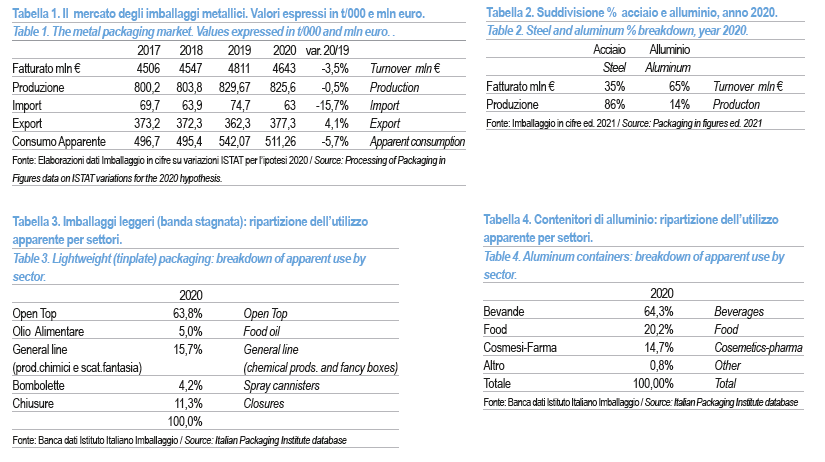

Among the longest-lived types of packaging - they have been on the market since 1800 - metal packaging in 2020 reached a total production in Italy of 825,600 tons, registering a drop of 0.5% compared to 2019: a result that, in a year like the one just ended, is undoubtedly of great importance.

Production was supported by exports, which grew by 4%, while imports were significantly down, closing 2020 with a negative trend (-15.7%). Apparent consumption dropped by 5.7%.

Out of total metal packaging, the representativeness of the two types of material changes depending on whether we are talking about quantities expressed in weight or turnover values. In the first case, steel packaging covers 86% of Italian production, while aluminium packaging accounts for 14%.

If we talk about representativeness expressed in value, the situation is reversed: aluminum packaging accounts for 65%, while steel packaging accounts for 35%.

On the basis of the first calculations available at the time of writing, the overall turnover of the metal packaging sector was down by 3.5%.

In a particular year, as 2020 has been, metal packaging has however recorded respectable numbers. Their link with the packaged food sector, mainly sold in large-scale distribution, has meant that use and production have not experienced the negative trends that have characterized the entire Italian and world industry. The sectors that suffered the greatest slumps in the food sector were those most closely linked to the HoReCa sector, with the obvious consequences for the packaging area (whose most negative performance, however, was recorded in the non-food sectors).

Another aspect not to be underestimated in the analysis of packaging is the trend in the cost of raw materials. With reference to 2020, after a first part of the year that recorded fluctuating trends but with substantially calm rhythms, in the last two months the waters have become agitated, showing significant increases. As regards both steel and aluminium packaging, raw material prices have soared since November, with a trend that has continued into the first part of 2021.

From the beginning to the end of 2020, steel scrap recorded a growth of around 9% (December over January), while aluminum prices recorded a December over January growth of around 2%.

For aluminum scrap the growth is decidedly different for the various types: the quotation for unalloyed aluminum scrap (UNI EN 13920/2) grew by 24% December on January; the quotation for scrap consisting of one single wrought alloy (UNI 13920/4) in the same period grew by over 6%.

Metal packaging has one of the highest recycling start-up rates: in 2020 79.8% of steel packaging released for consumption was sent for recycling; as regards aluminium packaging, the percentage sent for recycling was 67.7%, rising to 74.2% if energy recovery is also considered.

Steel packaging

Types and destinations of use

According to the classification used in Imballaggio in Cifre, steel packaging can be divided into two macro-categories: light tinplate packaging and thin sheet drums.

In turn, tinplate packaging is divided into three types:

• open top (tins used to package food products, such as peeled tomatoes, canned vegetables, tuna);

• general line (cylindrical and rectangular cans, truncated-cone and cylindrical buckets, bins, drums, with capacity up to 40 kg. Mainly intended for the chemical and food industry);

• closures (crown caps and twist-off caps).

Drums are instead made of sheet steel without tin coating, but protected by a suitable internal and external painting. Their capacity varies from 50 to 300 liters, with a clear prevalence of those with a capacity of 200 liters. They can be cylindrical or truncated conical and are used in the food industry (for example, for the handling of tomatoes from harvesting to processing) or, again, for the packaging of oil for industrial use, or non-food, petroleum, fuels, etc..

Size and characteristics of the Italian market

In 2020, the Italian production of steel packaging recorded a slightly declining trend in terms of production expressed by weight (-0.5%), reaching 708,100 tons compared to 711,900 tons in 2019.

The positive trend of both exports (+5.5%) and imports (+6.6%) should be highlighted. Apparent consumption drops by 3.8% (according to data from the Istituto Italiano Imballaggio there is no stock movement, so consumption is the result of the mathematical formula production+import-export and, for this reason, is defined as apparent).

The sector’s performance was sustained by the light tinplate packaging sector; open top, closures and part of the general line packaging (those of smaller dimensions) countered the negative trend of the Italian manufacturing sector, registering an increase in production of around 5%.

Open-top packaging, mainly used to package canned food, grew thanks to the increase in demand for these foods, especially in the lockdown period. This type of packaging represents about 63.8% of total light tinplate packaging and has registered a 2.5% increase in production.

The same reasons are also behind the increase in twist-off closures and capsules, also used in the canned food sector. Overall, steel closures, which account for 11.3% of light tinplate packaging, grew by around 3% in 2020. Edible oil containers also contributed to the positive trend, accounting for 5% of the segment, with growth of more than 10%. Canisters accounted for 4.2%.

The increase in light packaging production was supported by both domestic and foreign markets, with exports growing 6%.

Considering only chemicals and fancy cans (and therefore excluding edible oil cans and cans), general line packaging accounted for 18.6% and in 2020 recorded a decline of about 15%.

The steel drum area expressed a production of 109,000 tons, recording a further -2.2% compared to 2019.

Imports decreased by 7% while exports grew by 1.6%. About 70% of steel drums are used in the petroleum chemical sector, while the remaining 30% are used for handling seeds, tomatoes, or transporting products for industry. Apparent consumption is down 5.5%.

Aluminium packaging

Types and destinations of use

In the case of aluminum packaging, we are talking about various containers for food and non-food, beverage cans, cans for canned food, trays, in addition to tubes, used both in food and non-food (tomato paste, sauces, paints, cosmetics).

There are also aerosol cans and bottles used mainly in the cosmetic sector, as well as thin aluminum foil and closures (screw caps, easy open, etc.).

Size and characteristics of the Italian market

The aluminum used for the production of packaging includes can stock used for the production of beverage cans, foil stock used both in the production of thin foil and in the production of capsules, can bodies for food cans and tablets used for the production of cans.

The alloys that make up the various products are countless and vary according to the type of production and different uses.

On the basis of the analyses highlighted in Packaging in figures, in 2020 production expressed in weight decreased by 0.3%, settling at around 117,460 tons.Foreign trade, mainly influenced by the decisions of multinationals that are very present in this sector, registers a drop of 5.6%. Imports also fell considerably (-48.6%). This is explained by the fact that, often, multinationals with sites in different countries plan their production according to favorable market policies, moving it from one site to another; therefore, the material is imported, even if produced by the same company but in another country.

The strong drop in imports is reflected in an important way in the trend of the domestic market, with an apparent consumption at -12.3%.

Analyzing the segmentation in the different types of aluminum packaging, the following emerges.

27% of domestic production is represented by beverage and food cans (in 2020 at -3.9%). There is no doubt that the suspension of public events, concerts and festivals has led to serious losses in the cans sector.

Overall, the item “thin foil” (foil for wrapping and foil for yogurt pot closing), which represents 11% of production, grows by 1.6% in 2020 compared to 2019.

In contrast, closures remain fairly stable (+0.1%). The shutdown that affected the HoReCa sector significantly influenced the trend, as this type of closure is mainly used for glass bottles intended for the packaging of mineral water, spirits, soft drinks. Trays also fell, closing with a 3.2% drop.

In 2020, 64.3% of aluminium containers were used in the beverages sector, 20.2% were used in the food sector (including pet food), 14.7% were used in the cosmetics and pharmaceutical sectors, while the remaining 0.8% was represented by other items.

In conclusion

We can say that, among packaging, metal packaging has undoubtedly withstood better than others the impact of the pandemic that characterized 2020 and will greatly influence 2021.

We know that, at a general level, the packaging sector as a whole has responded dynamically and positively to the situation, but metal packaging, and even more so aluminium packaging, have distinguished themselves for their great ability to react in facing the extremely difficult situation.

Barbara Iascone

Istituto italiano Imballaggio