Report on the state of packaging – Data 2020 (1)

Four-monthly observatory of the packaging supply chain: situation updated at the beginning of December 2020.

NOTE

The data used to prepare this report is drawn from the Istituto Italiano Imballaggio.

This analysis starts from an examination of the FMCG sector, i.e. those goods that are commonly included in household expenditure, starting from food products, passing through personal and household care products, up to semi-durable goods, clothing, communication (books and newspapers)... in short, this is an area where the use of packaging is very high.

We will analyse the main sectors in detail below but, in general, the FMCG trend in 2020 managed to stem the losses, above all thanks to the possibility of purchasing these products from large-scale retailers - which never stopped - or thanks to online sales.

There was a drop, but it was decidedly less than the overall drop, standing at -7%, where it can be seen that the positive trend in household cleaning products was not able to offset the drop in cosmetics. It should be noted that household consumption rose by 6% for domestic cleaning products alone.

Food and beverage industry

In 2020 the food and beverage area has certainly stemmed its losses, becoming among the best performing sectors of Italian manufacturing, although not showing positive trends. There is no doubt that the upswing in domestic purchases has not been able to make up for the large losses suffered by the Ho.Re.Ca. sector, but it has certainly supported the industry’s production trend, especially in the food sector. The consumption of Italian families alone will see a growth of 2.6% in 2020; on the other hand, as far as production is concerned, which includes both goods for domestic consumption (families + Ho.Re.Ca) and exports, the trend for 2020 is -2.8%: a very limited loss, especially if we look at the trend of the entire manufacturing sector.

For the two-year period 2021-22 production is expected to grow by over 3% a.a.

Pharmaceuticals

In 2020, the pharmaceutical sector is the only sector of the manufacturing industry to show a positive trend, with production growing by +3.9%. World demand is driving the sector, while domestic demand is in slight contraction.

Growth for the two-year period 2021-22 is expected to be around +3%.

Household appliances and electronic products

These product categories also managed to contain losses, registering -7% and -8.9% respectively. Electronics benefited from digitalization incentives, made necessary by the massive recourse to smart working and distance learning.

Building materials

According to Prometeia’s analysis, building materials are expected to register a -10.5% in 2020. The sector has been helped by the restart of investments in construction, especially by the incentives provided for environmental building requalification: without these interventions, the drop

General economic picture

The year 2020 has just come to an end, a year that is, to say the least, unusual with trends never seen before at a global level. The general economic picture confirms widely shared expectations, with world production falling by 4.4% (latest analysis available from the International Monetary Fund, October 2020). If forecasts see the United States registering a drop in production in line with that of the world (-4.3%), the drop in production in the Euro Zone is decidedly greater (-8.3%). As far as emerging countries are concerned, the drop should be around 3.3%. Forecasts for 2021 are for a so-called “rebound” recovery, assuming that world production will grow by 5.2%. The trend for the United States will be +3.9%, while that for the eurozone will be +3.1%. Emerging countries are expected to register +6%. As far as GDP is concerned, according to the latest calculations available carried out by the International Monetary Fund, at world level 2020 will close with a -5.8%, with the United States registering a -4.3% and the eurozone a -8.3%. Italy will close 2020 with a GDP down 10.6%. For 2021 it is assumed that world GDP will grow by 3.9%, for the USA by +3.1% and for the eurozone by +5.2%. Italy will be in line with the European trend, registering a GDP growth in 2021 of 5.2%.

According to Confindustria

Also according to the analysis of Confindustria, the 2020 of the Italian economy will be marked by significant declines in all areas, causing negative effects on 2021, the year in which we will see a recovery but certainly still harnessed by the aftermath of the pandemic.

Consumption falls, the rate of mistrust of families increases, leading to an increase in the propensity to save. Exports fall as well, in October marking a 1.3% decline after having registered upswings in the previous five months.

According to Prometeia

Prometeia’s report (last update available October 2020) confirms that in Italy, during the summer months, there was an effective recovery, intense and spread among the different activities of the manufacturing industry, which was better than what was registered at European level.

In addition to the already positive results of the pharmaceutical sector, and the moderate drop in the food and beverages and FMCG sectors, other Italian manufacturing industries, such as the household appliances, furniture and building materials sectors, also recovered during the summer period, thus stemming the losses suffered in previous months.

That said, 2020 closes with a production in manufacturing equal to -14.3%.

For the two-year period 2021-2022, Prometeia forecasts a significant rebound in the sector, registering an average annual growth rate of turnover expressed at constant prices of +6.8%.

Justifying the positive sentiment is certainly the expectation of better management of the Covid-19 emergency, which would result in a brighter trend in demand and, consequently, in the production of manufacturing goods.

Driving this recovery will not be so much consumption as investments, which will be made thanks to European funds put in place to combat an economic crisis of epochal proportions.

However, Italian consumption will still be stagnant, due to a more cautious attitude ascribed to the deterioration of incomes.

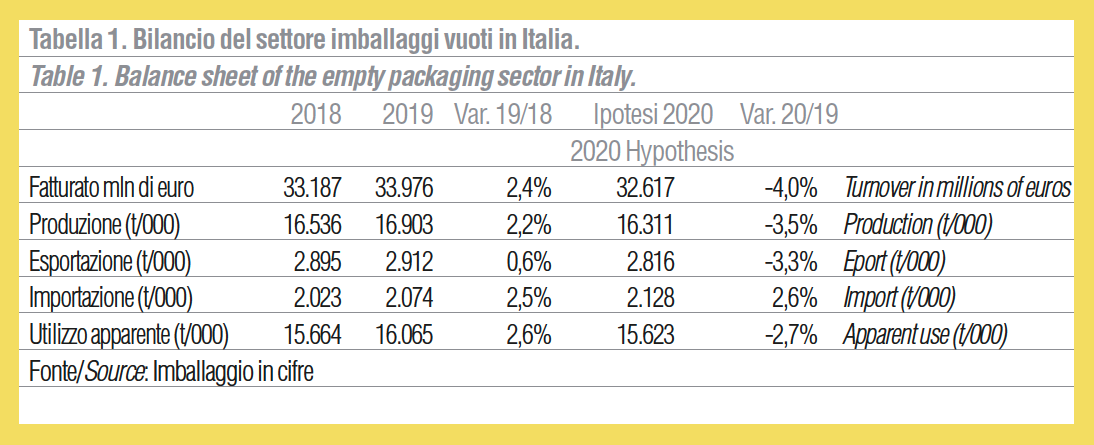

The packaging sector

After the overview of the manufacturing industry, which is a fundamental thermometer to assess where the packaging sector will be heading, let’s analyze what we hypothesize for the trend of the packaging sector in Italy.

On the basis of the first assessments of the trend in demand for packaging deriving from the various sectors of use, we hypothesize that 2020 may close with a turnover down by about 4%, reaching just over 32.7 billion euros.

Quantitative data expressed in tons show a drop in production of 3.5% where, to reduce the losses, the trend of the user sectors contributes. If, in fact, on the one hand, the manufacturing industry expressed highly negative trends, on the other hand, the “large users” of packaging managed to stem the losses, while still keeping Italian packaging production vital.

The Italian production of empty packaging is expected to reach about 16,300 t/000 in 2020. Exports should close with a drop of 3.3%, while the trend of imports is positive, +2.6% compared to 2019.

Raw materials: quotations

Regarding the average price quotations of raw materials used to produce packaging, in 2020 there are generalized decreases for all materials.

Starting from cellulose raw materials, prices for corrugated cardboard packaging will be down 6%, while those for bags and wrapping paper will be down around 9%; cartonboard will register an average price drop of around 0.8%. As far as paper from recycled sources is concerned, the average drop in prices ranged from -15% for “White cardboard without pulp” to -4% for “White trimmings”.

Prices of plastic polymers also fell. Of particular note was the 29.3% drop in PET prices and the average drop of 25% in Nylon prices.

There was a further average drop of around 20% for polyethylene, 19% for polystyrene and 11.4% for PVC.

On the other hand, prices of polymers deriving from recycling are very diversified. They range from an average -10% for HDPE granules to +9% for PP granules.

The price of blue rPET fell by 7% and that of multicolor rPET by 2%.

As far as metals are concerned, the average drop in the quotations of the raw material aluminum is around 3%, and aluminum from recycling is down by 4%.

Scrap steel shows around 40% drops.

Wood prices show an average decrease of 4%, while glass prices are stable.

Development hypotheses 2021-22

On the basis of the hypotheses of the user sectors, in the two-year period 21-22 the packaging sector should register a +3% both as regards turnover and production expressed in tons.