Report on the state of packaging – Data 2020 (2)

This report provides a cross-section of the trends in the sectors of the manufacturing industry where packaging consumption is most intense - and their consequent evolution - divided into food and non-food macro-areas.

This report provides a cross-section of the trends in the sectors of the manufacturing industry where packaging consumption is most intense - and their consequent evolution - divided into food and non-food macro-areas.

The evolutionary frameworks of the manufacturing sectors have been taken from sector analyses drawn up by trade associations, the data bank of the Italian Packaging Institute or Prometeia.

Food & Beverage. Compared with the analyses referring to the first eight months of the year, the food and beverage sector managed to stem losses by a considerable margin, ending 2020 with just -0.6%. Largescale distribution and online shopping have ensured that the sector has been able to counteract the collapse in consumption in the HoReCa sector (over -37% by volume). In 2020, online sales in the Food & Grocery area grew 55%. For the 2021-22 biennium, production is expected to grow more than 3% a.a.

Pharmaceuticals. After the positive growth rate reported for the first 8 months of the year (+3.9%), the pharmaceutical sector closed at -0.9%, with the sharpest declines recorded at the end of the year.

FMCG. his sector includes all goods for domestic use that are commonly purchased from largescale retail outlets, including food products, personal and household care products, as well as “semi-durable” goods (clothing, books and newspapers, etc.). In short, this is a vast area with “wide use” of packaging.

In this case too, as for the food and beverage sector, the end of the year brought with it some improvements, reducing the losses recorded in the first 8 months of the year. For FMCG, 2020 therefore closes with a -4.1%.

It should be pointed out that the sector suffered from the lack of a “driving effect” in cosmetics, which in 2020, due to various restrictions, recorded significant losses in relation to both domestic and foreign demand.

Household appliances. Here too there was improvement towards the end of the year: 2020 closed at -3.1%.

Furniture and furnishings. The sector managed to recover the -18.5% forecast in December; the recovery of exports referred to the last months of the year allowed to reduce losses (-8.9%).

Building materials. Also thanks to the numerous incentives, building activities recovered, positively influencing the market of construction products and materials, which close 2020 at -6.6%.

Cosmetics and perfumery. Analyses conducted by the Cosmetica Italia study center report a decline in 2020 of 12.8% (a few percentage points have been recovered compared to the preliminary figures, which showed a drop of over 15%). Exports - which alone dropped by 16.8% - are still heavily influencing the production trend.

Chemicals. In 2020, chemical intermediates contained their losses to -9.2%, due to the demand for chemical products for the production of sanitizers.

Fashion system. The fashion industry confirms the expected declines: in 2020 the trend drops to -21.6%.

Quadro economico generale

The final trends of the 2020 macroeconomic indicators all register a minus sign, except for the unemployment rate which closes with +9%. The data processed by ISTAT tells us that GDP in Italy in 2020 closed at -7.8%, industrial production at -5.4%, with domestic demand and household spending falling (both) by 9.1%.

But recording the most significant drop among all macroeconomic indicators is manufacturing activity, which closes with 2020 turnover at constant prices at -10,2% .

According to Confindustria. Nelle In the latest surveys provided by the sudi center of Confindustria, 2021 begins with some very slight recovery. After recording +0.9% in the first quarter, industrial production is confirmed to be recovering, albeit at reduced rates, with +0.5% in the second quarter of 2021. Production, net of the different number of working days, increases in both May (+22.6% compared to the same month in 2020) and April (+73.2%), but this wide range must be considered in relation to the first months of the 2020 pandemic, where the production stoppage had been almost total. The progression of the national vaccination plan, with the corresponding decrease in contagions, is giving rise to a progressive improvement in the economic sphere thanks to the easing of restrictions and a resumption of travel: the true lifeblood of the Italian economy..

According to Prometeia. As already anticipated, the trend in manufacturing activity will record a drop in 2020 of -10.2%; compared to other crises in the past, this one is undoubtedly anomalous, generated by pandemic alarm and not by economic reasons. In spite of the lockdown that characterized 2020, with a very extended production stoppage, the drop translated into a trend that was much better than expected (consider that the drop in manufacturing activity in 2009, the year of a purely economic crisis, was -18.8%). Thanks, therefore, to the recovery in turnover in the period August-November, losses were in fact reduced. The domestic dynamic was better than the foreign one, at +0.7% and -2.4%, respectively. In general and according to the latest available data, there are many sectors of the manufacturing industry that have reduced the gap with 2019 at the end of the year. Among these are the sectors most closely tied to the packaging industry.

The packaging sector

After the overview of the manufacturing industry, which is a fundamental thermometer for assessing where the packaging sector will go, let’s examine what we assume to be the trend of the packaging sector in Italy.

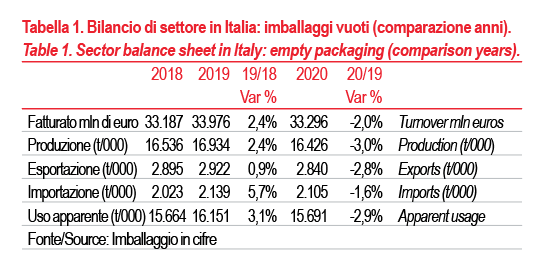

In 2020, packaging production (including MSW bags) expressed by weight is expected to settle at around 16,415 t/000, marking a decline of around 3% compared to 2019.

Turnover, which is expected to be around 33.2 billion euros, would be down by 2%.

The strong link with the FMCG and food sectors is thus reconfirmed, which has made it possible to contain the falls compared to the rest of the Italian industry.

Within the various materials, it is paper and cardboard packaging that is strongly countering the negative trend, thanks to the trend of online sales of goods (+30% in 2020). Cellulose packaging alone grows by about 1%, achieving an extremely positive result in an annus horribilis such as 2020.

All types of packaging linked to canned food packaging also managed to give positive inputs to the sector.

Foreign trade was down, with exports of packaging falling more than imports, according to ISTAT data (-2.8% and -1.6% respectively). The trade balance remains positive, with a value of about 746,000 tons; in practice, we continue to export more than we import, although this gap is steadily decreasing: in 2020, the trade balance is down by -6% compared to 2019.

Apparent utilization, which does not take into account the movement of inventories, drops by 2.9%.

The area with the highest trade volume remains Europe, with a significant increase in imports from Poland and Turkey.

As far as the prices of raw materials used to produce packaging are concerned, the price trend shows a certain uniformity: the prices of all materials followed a swinging downward trend in the first 9 months of 2020, only to surge towards the end of the year. Raw material price increases continue in 2021.

Evolutionary assumptions 2021-22. Based on initial analysis for 2021, we assume a slight recovery for the sector, although it will be unlikely to fully recover the losses accumulated in 2020. The assumption is for production to grow by 1%. With an average annual growth rate of +0.4% in 2023 we should recover and exceed the tons of packaging produced in 2019.

Barbara Iascone

Istituto Italiano Imballaggio

NOTE: The data used to elaborate the report are taken from the Istituto Italiano Imballaggio database.