Report on the state of packaging – June 2013

The quarterly packaging chain observatory. Situation at the end June 2013

Here at a glimpse the performance of the manufacturing industry sectors where the level of packaging consumption is the most intense, divided into macro areas of food and non food. The prospected growth picture of the manufacturing sectors has been drawn from the sectorial analyses made by the sector associations or by Prometeia.

Food industry Food and drink

According to Prometeia, the food industry is experiencing a drop in production that started in 2011. Year 2012 also ended with a drop in production of 2.2%: the downturn essentially stemming from the heavy drop in household consumption, back to the levels of the mid-90s.

Exports continue to show some growth, thanks to demand from the emerging countries.

Also according to Prometeia’s ratings, 2013 will feature a slight recovery in production of 0.3% thanks to exports, while a further drop in domestic demand is expected. In the food area, after the decline in production of 1.5% in 2012, in 2013 a further downturn of 0.8% is on the cards for the food segment. Even the beverage sector shows a downturn in terms of production: -6.3% in 2012 and -0.3% in 2013.

Non-food Pharmaceuticals

During 2012 the pharmaceutical sector was also affected by the economic crisis; according to Prometeia, production registered a slight subsidence of 0.3% and the increase in exports failed to offset the reduction in demand.

The decline in domestic consumption is derived both from Italian state healthcare cost containment, as well as due to reduction in purchases of non-reimbursable products and by a contraction of 5% of the sales of OTC pharmaceutical products.

For 2013 a further decline in production is also expected, as ever due to a reduction in domestic consumption not offset by the limited growth in exports.

The fashion system

After ending 2012 with a drop in production of 5.5%, according to Prometeia the activity of this important manufacturing area will register a further drop of 2.3% for 2013. The sector is aboveall weighed down by the drop in domestic consumption, the greatest witnessed over the last 40 years. Added to the difficulties of the domestic market one has problems involving exports - down 4.2% in 2012 with the forecast of modest +0.6% in 2014.

Cosmetics and perfumery

Having emerged virtually unscathed from previous economic crises, in 2012 the sector suffered a downturn, especially in terms of domestic consumption, which showed a drop of 1.8%.

Exports on the other hand managed to end the year with an optimistic (+7.1%), to the point of concluding 2012 with a slight increase in production (+0.9%).

According to Cosmetica Italia (formerly Unipro), the growth potential for 2013 remain moderately positive for exports headed for areas outside the EU, while a drop in domestic demand is forecast. All things considered, the sector as a whole will be able to reconfirm figures for 2012.

Furniture and furnishings

Prometeia estimates speak of a drop in production of 11.6% in 2012, with the outlook for 2013 indicating a further decline of 5.3%.

The industry has been in a crisis since 2011, both due to the progressive reduction of domestic consumer spending and to the drop in exports.

The sector what is more is witnessing a singling out of the less competitive concerns, particularly with regard to exports, which stand as the true growth driver in that they account for 40% of production.

As for domestic demand, a sizeable and continuous decline is underway since 2011. Italian manufacturers are suffering most, conditioned among other things by competition from Ikea.

Chemical products

On the basis of figures processed by Federchimica (and with reference to the values showing volume by the chemical industry), in 2012 Italian domestic consumption fell by 5.5%, exports were down by 1.5% and imports by 5%.

Production is down by 4%.

For 2013 a recovery in production is expected, although limited to 0.6 -1%, mainly fuelled by exports. Italian chemical industry foreign trade, based upon the early months of 2013, presents a promising trend, which leads to growth estimates of 2.4%. The growth in exports is due to the segment having been able to hook up to the growthtrend of the markets outside Europe.

Mechanics

In 2012, according to Prometeia, this manufacturing area showed a drop in production of 4.1%, due to a 12% drop in domestic demand and a drop in exports of 2.2%.

2013 should still see a recessionary trend, down 1.5%, due to a further reduction of domestic demand, not compensated for by exports (the latter will not go beyond a +2-2.3%).

Household appliances

Production has been progressively declining since 2010, well before the current global economic recession. Sizeable the further decline in production registered by Prometeia in 2012 (-9.5%) while 2013 should see a further drop of 3.6%.

Decline in domestic demand and the drop in exports are at the origin of the negative trend. The segment has been heavily affected by the transfer abroad of production and by increased imports (both of products from the Italian companies that have moved their facilities abroad, both due to import flows to Italy from foreign competitors).

It is considered that this manufacturing area will have great difficulty in recovering.

Building materials

This sector has suffered an ongoing downtrend for years, conditioned by the extensive and heavy drop in the activity of the construction industry.

From 2008 to 2012 a drop of over 20% was witnessed, and in 2012 the downturn was 6.2%.

Confirmed by Prometeia, construction materials (cement, glass, ceramics, lime and rebars) are obviously affected: in 2012, they suffered a -11.9%, compounded in 2013 by a further -3.5%.

According to assumptions a recovery should take place between 2015 and 2017.

The economic picture

2013 got off with foreboding signs of a persistent downturn at European level, Italy being particularly affected.

In Italy domestic demand shows no signs of recovery and exports, although tending to grow, are incapable of offsetting the downturn in production.

Surveys made by the Confindustria Study Center showed a decline both in production and order bookings for the first two months of 2013.

Various ISTAT indicators confirm that the weakness of the manufacturing industry shall persist in the months ahead; hence the first half of the year will in all probability feature a downturn.

However, the prospects of a possible turnaround in the manufacturing industry in 2013 have been reconfirmed both by Prometeia and by other market analysts, such as the Confindustria Study Center, though it will not be such as to allow an upturn in the overall yearly GDP figures.

What with a possible slow recovery setting in in the autumn, it is believed that the Italian GDP will show a slight decline of around 0.5-1% and manufacturing activity should put in limited growth at 0.4-0.5%.

In addition these prospects are subject to a reversal of the current recessive economic cycle by the third quarter of 2013.

It is believed, however, that the recovery can only be driven by exports and a replenishing of stocks, currently at very low levels. Italian domestic demand, at best, will stabilize at the current low levels, in particular food consumption should pick up, albeit slowly, while for non-food consumer goods a further drop is deemed likely.

The manufacturing industry, according to the Prometeia calculations made in May, 2013 should feature the following changes:

production -2.2%; imports -1.5%; exports +1.6%; domestic demand -3.2%.

Other sources unfortunately report a greater decline in Italian domestic demand, which will substantially involve both imports as well as sales nationwide. All analysts are oriented towards locating the beginning of a true recovery during the year 2014.

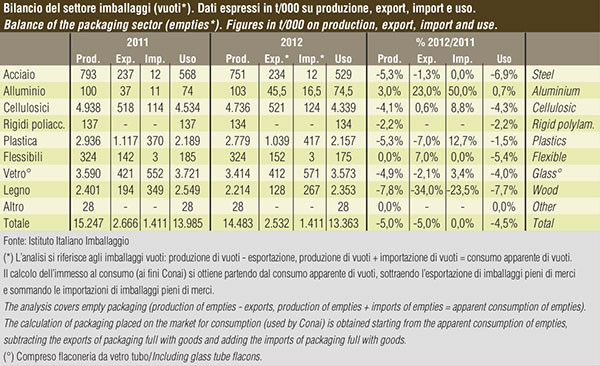

Packaging: how much is produced

The year 2012 closed with a 5% drop in production and 4.5% drop in domestic demand in figures expressing weight.

Foreign trade had also declined, showing a drop of 5% in exports and with imports substantially stable.

The only areas that in 2012 showed an upturn or that didn’t show a drop (figures for production in weight), were aluminium packaging (+3%) and flexible converter packaging, that reconfirmed 2011 figures thanks to the excellent run of exports.

During 2012 the growth trend of raw materials for packaging production was decidedly low (though it should be remembered 2011 showed significant increases).

During 2012 sector turnover reached 29,3 billion euro, and set against 2011, put in an increase of 15.5%.

The growth prospects for 2013 for the Italian packaging industry are currently not encouraging, given the continuing economic crisis that, does not show any signs of abating.

NOTE. The data used to compile the report is drawn from the Istituto Italiano Imballaggio database.

Edited by Plinio Iascone

Istituto Italiano Imballaggio