Health packaging

Facts and figures on the Italian market and on the packaging of the various pharmaceutical forms: an analysis of medicinal products for human use (ethical and OTC) sold in pharmacies, excluding products consumed in hospital.

According to Prometeia, the pharmaceutical sector as a whole (OTC products, including hospital products and excluding veterinary drugs) in the years 2013 and 2014 showed an increase in sales of +2.5% and +0.7%, hence going against the tide of the general decline in production in the manufacturing industry.

The situation was mainly driven by medicines for export, up 16% in 2013 and by 5,9% in 2014.

The growth in exports has continued to be driven by very intense “intra-company” exchanges between multinationals.

Still according to Prometeia, during the 2013-2014 period, Italian domestic demand registered a modest growthrate (average rate of 0.5%) compared to an average growthrate of around 1,5-1,7% of the two years 2011-2012.

Federfarma reports that, in the last two years, national Italian consumption of pharmaceuticals has shown an annual average decline of 2.3% in terms of value while showing an annual average growth of around 2-3% in terms of quantity (in practice with reference to reimbursable drugs).

Federfarma believes that the decline in value results from the repeated cuts in drug prices, after the expiry of the patents of many medicinal products that have been replaced by more inexpensive equivalents.

The growth prospects for 2015, according to Prometeia’s ratings, are moderately positive, with exports showing growth and a slight improvement in the trend in domestic demand.

Packaging in figures

The packs placed on the market can be divided as follows:

- 87% accounted for by class A, B and C ethical products of (according to Italian Ministry of Health categories);

- 2% by other ethical products sold without prescription;

- 11% by OTC pharmaceutical products,shown to be on the increase.

It is estimated that, in 2014, the market area in question (ethical and OTC drugs sold in pharmacies) accounted for 2,081 t/000 packs, totaling approximately 1,118,000 packs, up 0.5% compared to 2013 .

From 2000 to 2014 the Italian consumption of ethical (prescribed) drugs and OTC products grew by a 2.2% annual average.

The number of packs sold in 2014, with reference to the main pharmaceutical forms has reached the following quantities:

- 624.3 t/000 packs involving liquid pharmaceutical forms (injectable, oral, ophthalmic, etc.), showing a drop of 2.7%;

- 1331.8 t/000 up 2.1% involving solid pharmaceutical forms (tablets, capsules, powders etc.);

- 124.9 million involving other types of drugs (ointments, gels, sprays etc.), showing an increase of 0.6%.

Sales of liquid medicines have long been mainly driven by injectables, following the spread of vaccination against influenza and those for newborn babies (of note that, over the last two years, births in Italy have been up due to the massive presence of immigrants).

In 2014 however the increase of injectable drugs came to a halt due to the significant reduction in anti-flu drugs, initially believed to be responsible for the deaths of some older patients (but the situation has gradually normalised).

The growth of solid dosage forms has been driven by orally administered drugs; lastly a slight increase has been seen with regard to other pharmaceutical specialties mainly featuring the growth of creams, gels, ointments and foams.

The packaging of the pharmaceutical forms

Packaging a pharmaceutical drug is a very delicate matter.

First of all packaging has to meet some primary functions: protect the product, ensure the absence of negative interactions between container and pharmaceutical product, render the use of the same easy and functional, hinder tampering and misuse.

The choice of packaging is obviously linked to the type of drug (liquid, solid, spray etc.), but also to the characteristics of the substances contained in the drug itself (as is known, the packaging of a new drug is subject to approval by the Italian Ministry of Health).

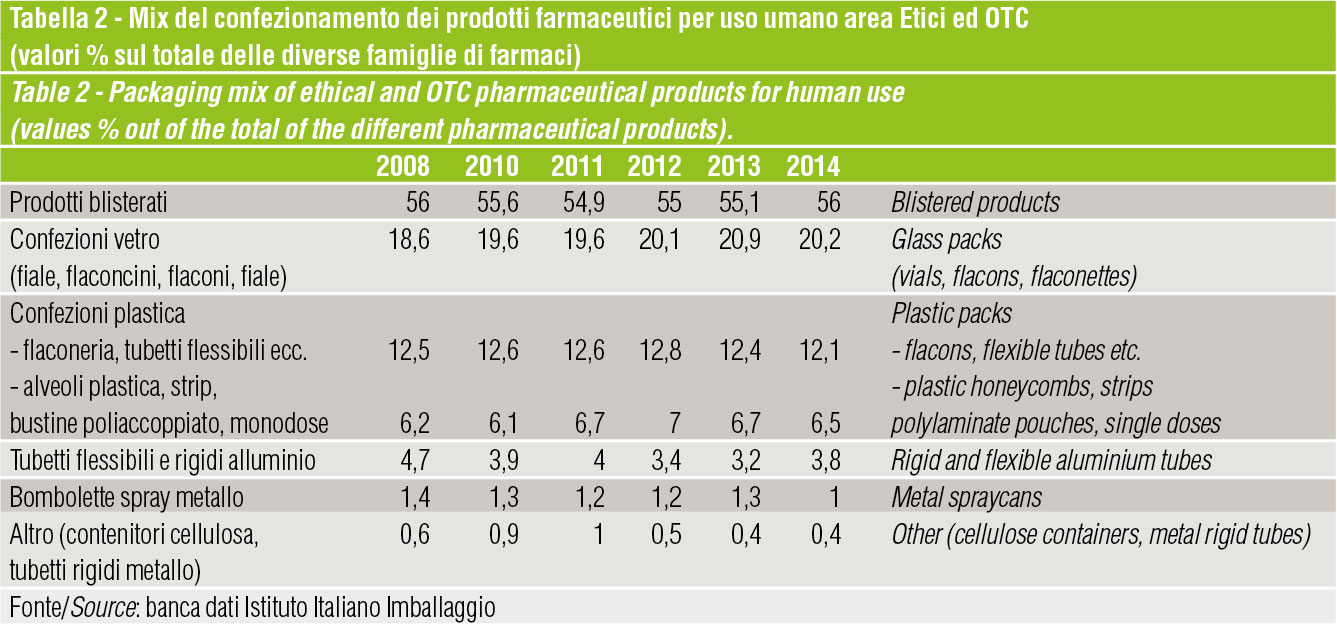

It is estimated that in 2014 2,081,000 million packs (+ 0.5% compared to 2013) were made for the various types of pharmaceutical products present on the market.

Interesting too the changing picture of the packaging mix (below the percentages on the totality of pharmaceutical containers).

- Blistered drugs have reached a share of 56% and are still growing steadily.

- Glass packaging (20.2%) is down slightly compared to 2013, due to the decline of injectable drugs.

- Plastic packaging (bottles, flexible tubes and dispensers) stands at 12.1%, tending to grow. Its use is 93% accounted for in non drinkable drugs (ophthalmic, otological etc.), drugs in solid form for external use (creams, powders etc.) accounting for a share of 41% and in creams and ointments accounting for share of 24%.

- Packaging in plastic or in flexible converter polylaminates (honeycombs, strips, pouches and microclisms) accounts for a share of 6.5%.

- Aluminum packaging (flexible and rigid tubes) stands at 3.8%. Creams and ointments account for around 66%, powders and granules 50%.

- Aluminum aerosols have a 1% market share. The main field of application is in sprays and foams (92%), where the alternative offered by the plastic bottle stands at 8%.

The other main type of primary packaging used for pharmaceutical products, with a share of 0.4%, are: flexible tubes in both plastic and aluminum, aluminum rigid tubes, cellulosic and spiral wound paper containers (used for the granular medicines for oral use).

An interesting trend can be seen in the greater tendency to use single doses, reaching a market share of 5% in the ophthalmic-otological area, 3.5% in oral-solids, 9% in drugs for external use and 10% in ointments and foams.

Obviously, in addition to the primary packaging, the packaging of pharmaceutical products also includes secondary packaging (carton boxes) and transport packaging (corrugated cardboard boxes, pallets, stretchfilm, etc.).

As far as folding cartons are concerned, their use is in fact necessary not only to protect the container but also to contain the leaflet showing the characteristics of the medicinal product and the instructions for use. All prescription and OTC drugs sold in pharmacies come in cartons (41,519 t).

Corrugated boxes and pallets are used to handle pharmaceutical products.

Plinio Iascone

Istituto Italiano imballaggio