Plastic packaging – Data 2014

Growth trend of production and market position. Plinio Iascone

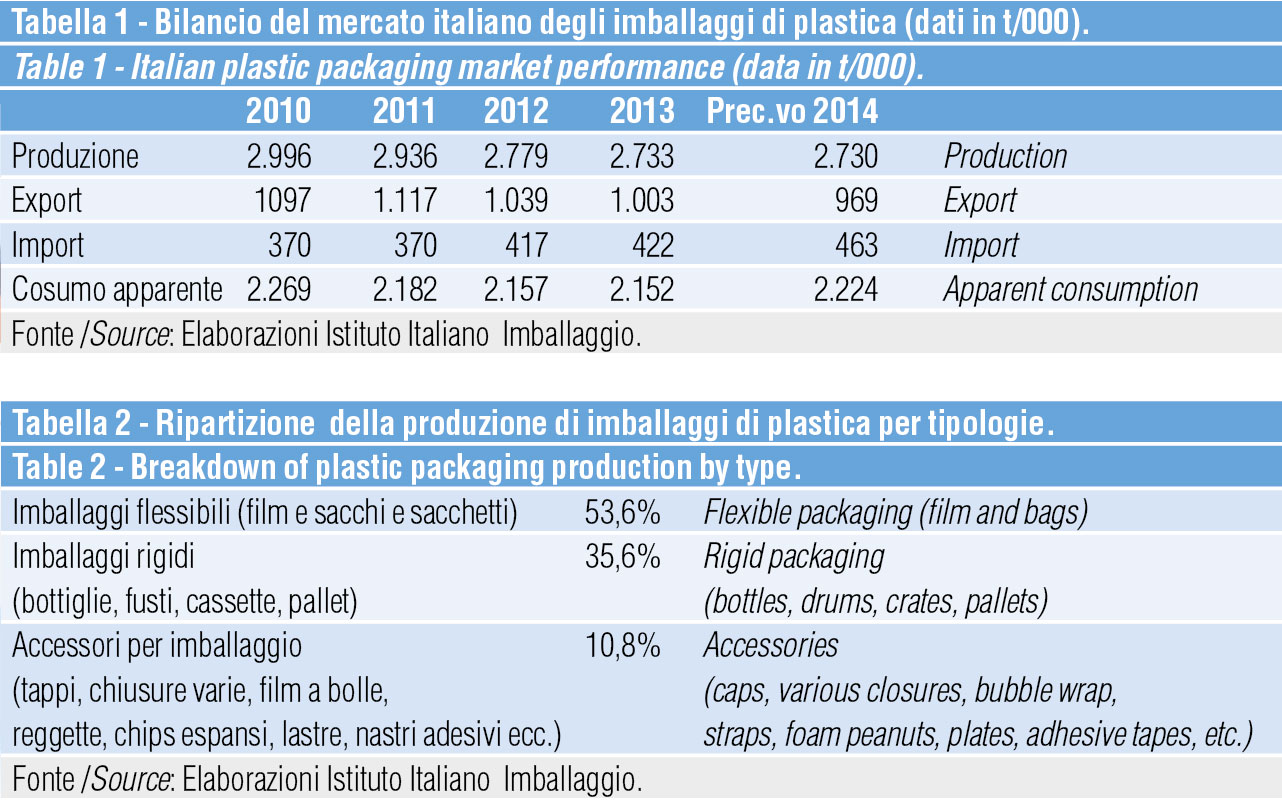

Due to the economic recession, and similarly to other types, plastic packaging has also experienced a decline in production, caused both by a drop in domestic consumption and by a re-scaling of export flows.

The following values emerge when looking at the trend from 2010 to 2013:

- a 5.2% drop in domestic consumption;

- a 9% drop in exports;

- a 14% increase in imports;

- a 9% drop in production.

Considering domestic demand, the growth outlook is even worse, especially when looking at consumption of Italian products, which dropped by 9%, to the benefit of import products.

According to initial estimates, the situation seems to have improved in 2014. Domestic demand has indeed recovered by approximately 3%, attributable to a +1.8% Italian products and especially +9.7% for imports.

On the other hand, exports have fallen by another 3%.

Production is expected to remain stable at the low levels reached in 2013.

It can nevertheless be surmised that the crisis that began in 2011 is slowly giving way, to the point that 2015 should see progressive recovery for the sector.

As for packaging production, in recent years there has been a slight progressive recourse to recycled materials and bioplastics. In the former case, 435,000 tons were used in 2013, destined to grow considerably in 2014.

As for bioplastics, they were destined mainly for the production of shoppers and wrapping films, reaching approximately 26,000 tons.

Areas of use and types

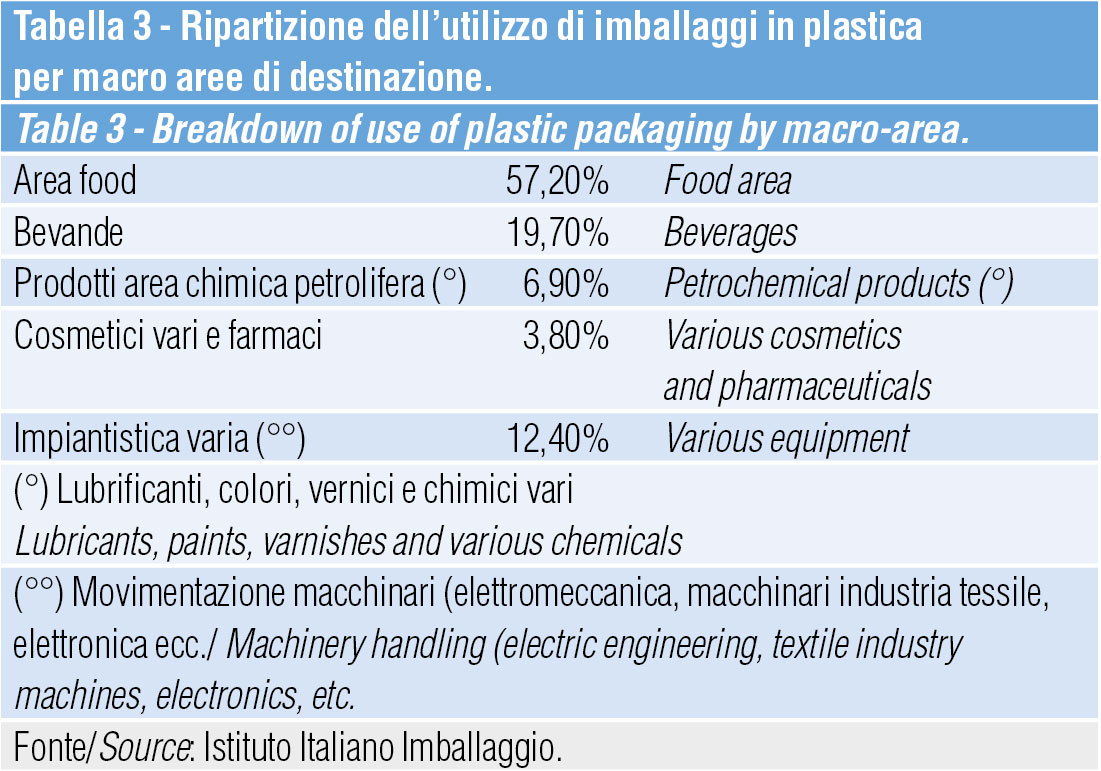

Plastic packaging represents 19% of total packaging production, but considering the reduced average weight of this type, the market share is certainly greater (23-25% of the total, by a wide margin of error).

Plastic packaging has countless sector applications, in handling food (fresh and preserved) and beverages, technical products and machinery… These can be divided into three macro-areas:

- flexible packaging (stretch films and bags);

- rigid packaging (bottles for beverages, bottles and flacons for technical products, bins, pallets and crates);

- packaging accessories (rope, straps, caps, hoods, filling material, chips, bubble wrap etc.)

The food sector accounts for the greatest share with 76% (54% food, 22% beverages).

A substantial proportion of plastic packaging (7%) is destined for the chemical industry (inks, paints, lubricants etc), while cosmetics and perfumes account for approximately 2%. In these cases, the breakdown of packaging uses shows a remarkable variety of packaging types, subject to innumerable changes. In the pharmaceutical sector, which uses 1% of plastic packaging, the changes in packaging are very slow, because they usually have to be authorized by the Ministry of Health.

There is a significant presence of plastic packaging in non-food consumer goods (6%). The remaining 8% refers to the use of plastic packaging for handling various types of equipment and machinery.

A cura di Plinio Iascone

Istituto Italiano Imballaggio