Report on the state of packaging – May 2015

A four-month survey of the packaging industry. The situation as of late May 2015. By Plinio Iascone

Below is a breakdown of the performance of the manufacturing sectors which consume the most packaging, subdivided into the macro-areas of food and non-food. A report on the evolution of the packaging sector will follow.

The performance histories of the manufacturing sectors, on the other hand, are taken from analyses conducted by sector associations or Prometeia.

Food industry (food and beverage)

According to Federalimentare, after three years of progressive decline, the sector ended 2014 with 0.6% growth in production, mainly determined by domestic demand in the food area; the beverage sector declined slightly.

The product types with the best performance are: fish products, products derived from processing and preserving fruit and vegetables, baked goods, flour-based products, confectionery, tea, coffee, spices, ready meals and baby foods.

Prometeia forecasted moderately positive trends: +1.6% in 2015, +1.4% in 2016 and a +1.2% yearly average for the three-year period of 2017-2019. The growth will be oriented mostly by exports, but domestic demand is also expected to tend toward recovery: +1.7% in 2015, +1.2% in 2016 and a +1% yearly average in 2017-2019.

Pharmaceuticals

For 2014, Prometeia analysis indicates a 1.1% growth in production. It must be pointed out here that, even in an unfavorable economic climate, domestic demand (driven basically by an aging population and increasing attention to preventive medicine) has continued to grow, albeit at more limited rates than in the past (+1.1%). Forecasts are for +1.8% in 2015, +2% in 2016 and an average yearly of +1.6% in 2017-2019.

Domestic demand, on the other hand, shows a more limited but sustained growth trend: 0.3% in 2014, 1.7% in 2015 and an average yearly rate of 1.4% in the four-year period of 2015-2019.

Fashion system

In 2014, the sector resumed expressing a positive growth trend (Prometeia data): production recovered by 1.8%, driven by exports, domestic demand reversed its trend (+0.7%), and imports are growing.

Cosmetics and perfumes

According to a periodic analysis conducted by Cosmetica Italia, in 2014 the sector’s production grew by 1.7% thanks to the good performance of exports (+7%). For the second time, on the other hand, the domestic market concluded the year in slight decline.

Expectations for 2015 are good, with further production growth driven by exports, but also some recovery of domestic demand..

Furniture and decor

Thanks to the recovery of the last quarter of 2014, the furniture industry resumed production growth at a rate of 0.3% (until autumn Prometeia had projected a further decline of 0.6%).

The correction “mid-stride” is due to rising exports, which ended the year with +1.8%. Domestic demand, on the other hand, continued to fall (-0.3%).

In both 2015 and the three-year period of 2017-2019 this recovery should consolidate itself, mainly thanks to exports, but also in part to greater domestic demand.

Chemical products

Federchimica data show that, following a very bad three years, the Italian chemical sector finished 2014 with a 0.8% growth in production, driven by exports (+2.8%). On the other hand, domestic demand has remained basically stable at the low values of 2013.

Also according to Federchimica, the recovery should continue to 2015: +1.4% production, driven by strengthening exports (+3.2%), but also a domestic demand that should reach 1.3% growth, after two years of decline. Imports should also tend to grow (+2.5%).

The development of the Italian chemical industry will always be tied to increased exports of high tech products.

Mechanics

Production still in decline in 2014, according to Prometeia, following a slowdown in both domestic demand and exports. By contrast, projections for 2015 are positive: +2.3% production, +3.2% exports and +3.3% imports, with a domestic demand of +1.8%, after two years of recession.

The progressive recovery of production should persist in 2016 as well as 2017-2019, driven by domestic demand and exports.

Electric appliances

During 2014, according to Prometeia’s findings, production in this sector has begun showing the early signs of recovery (+3.4%), driven by +2.3% imports.

And while domestic demand, by contrast, continues to falter, imports have undergone net growth (+8.5%).

The growth forecasts for 2015 and until 2019 are oriented toward a slow recovery of domestic demand, with a yearly average of 1.2%. Exports are expected to grow progressively: +2.6% in 2015, +2.5% in 2016 and +2.9% yearly average in 2017-2019.

Production should also be due for a recovery, albeit at decidedly lower rates, sustained only by exports, since the growth of domestic demand will be driven essentially by imported products.

Construction materials

The long recession of construction also continued in 2014, obviously involving construction materials (cement, concrete, bricks, steel rebars, etc.).

In the last six years, the decline of this sector’s production has been 26% (but the trend was by no means satisfactory in previous years).

Since 2015, according to analysis by Prometeia, business in the sector and that of construction materials has begun a gradual recovery process.

For the coming years, the following growth rates are expected for construction materials: +1.5% in 2016 and +1.8% yearly average during the three-year period of 2017-2019.

The general economic outlook

According to Confindustria, the Italian economy is doing better than expected. During the first quarter of 2015, the country’s GDP was +0.3% (the first growth since the third quarter of 2013), with a possible projection of +0.2% for the current year. Industrial production is also supposed to have ended the first semester with 0.8% growth. From September 2014 (when industrial production reached the lowest levels since April 2009) to March 2015, it grew by 1.4%, albeit with wide variations. 2015 could therefore end with +1.8-2%.

Prometeia also found that the Italian economy has ended a long recession (ten quarters in decline), as certified by its data on the GDP trend. Indeed, following the recession, manufacturing ended 2014 with +0.6% thanks to the recovery underway in the last quarter of the year, and both exports and imports grew, by 1.2% and 2.3%, respectively. Domestic demand registered a 0.2% recovery.

Also according to Prometeia, expectations are that the Italian manufacturing industry will show moderately positive growth and sustain a progressive recovery: +1.8% production in 2015, +2.1% in 2016 and 2% yearly average in the three-year period of 2017-2019.

Imports are also expected to grow: +2.9% and +3.3% in 2015 and 2016, and a yearly average of +3.1% in the three years of 2017-2019.

Projections also dictate a growth in domestic consumption: +1.7% in 2015 and 1.9% in 2016, +2.5% yearly average in the three years of 2017-2019.

It’s important to keep in mind that according to forecasts beyond 2016, manufacturing will largely depend on the growth of exports, since domestic demand will grow only modestly.

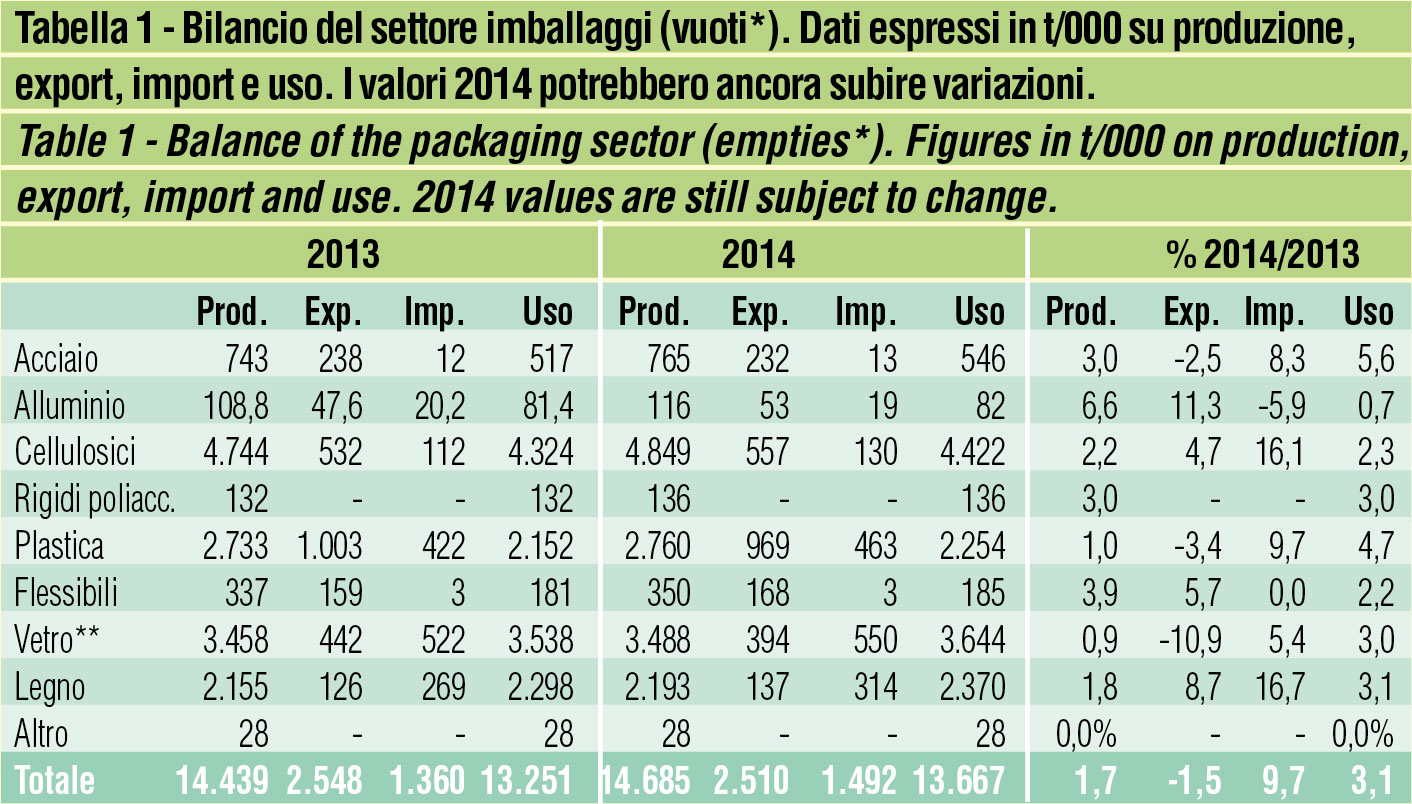

The packaging sector

2014 is supposed to have ended with a slight production increase of 1.7% in quantitative terms, following the progressive recessive trend of 2011-2013. It’s still too soon to confirm: the numbers are to be considered definitive only after publication of “Packaging in numbers” by Istituto Italiano Imballaggio, scheduled for late July 2015.

Looking at the growth trend of the packaging sector, the slight recovery can be attributed to the two months of November/December for most sectors.

The trend inversion is mainly driven by growing domestic demand, which is however determined by significant growth in imports (+9.7%). Exports, by contrast, have dropped slightly (-1.5%).

Production data for all packaging sectors evidence generalized growth: +3% for steel packaging; +6.6% for aluminium packaging; +2.2% for cellulose; +3% for rigid polylaminates; +1% for plastic; +3.9% for converted flexible polylaminates; +0.9% for glass; +1.8% for wood.

The packaging sector’s turnover, still according to initial estimates, grew by 3.8%: this figure is considered reliable, given the overall stability of raw materials.

Growth projections for 2015 are oriented toward slow but progressive growth in production, driven by both recovering domestic demand and exports.

(*)The analysis refers to empty packaging units (production of empties – export of empties + import of empties = apparent consumption of empties). The total put on the market (for Conai pruposes) is calculated from apparent consumption of empties, by subtracting exports of full packaging, and adding imports of full packaging.

(**) compreso flaconeria da vetro tubo / (**) including glass tube flacons

Fonte/Source: Istituto Italiano Imballaggio